Full Report

The numbers behind Molina Healthcare, Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ millions unless noted.

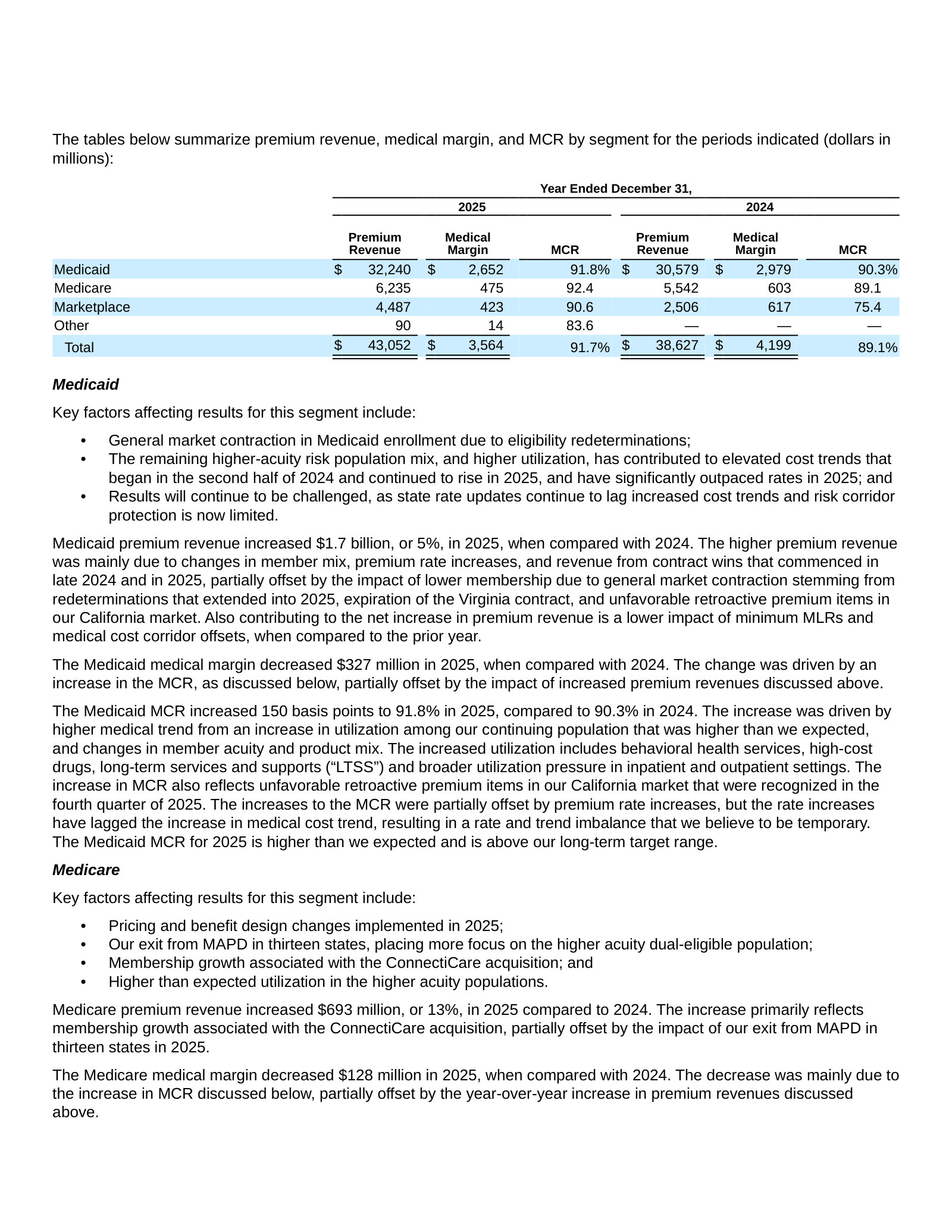

Reading notes: All figures in US$ millions as printed in the filings, except per-share (US$) and ratio/percent rows. Fiscal year ends December 31. Each FY2021–FY2025 column is cited to that year's own Form 10-K (income and cash flow statements print three years; balance sheets print two). Every core-statement cell in the FY2021–FY2025 columns is filing-verified. Revenue breakdown and medical margin are the company's reported segments — Medicaid, Medicare, Marketplace and (from FY2024/FY2025) Other — taken from the MD A 'Segment Financial Performance' premium/medical-margin/MCR tables. The 'Other' segment premium is reported only from FY2025 ($90M); it was nil or not separately shown earlier. Long-term record FY2016–FY2020 figures are from the standardized data feed (SEC XBRL) and are shown without page links; FY2021–FY2025 are filing-linked.

Share Price — Full Available History — 23 Years

The stock closed at $224.82 on Jul 16, 2026 — up 2,429% over the window shown (+15.1% a year), trading between $7.44 and $419.53. At that close the stock trades at 25× FY2025 diluted EPS as reported below.

Source: market price feed, monthly closes, sampled from 5,796 source observations, Jul 2003–Jul 2026. Price return only, excludes dividends. Prices are split-adjusted (×1.5 on May 23, 2011).

FY2025 at a Glance

Revenue (US$ millions)

Operating income (US$ millions)

Net income (US$ millions)

Diluted EPS

Source: FY2025 consolidated statements [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Premium Revenue by Program

| Premium Revenue by Program | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Medicaid | 20,461 | 24,827 | 26,327 | 30,579 | 32,240 |

| Medicare | 3,361 | 3,795 | 4,179 | 5,542 | 6,235 |

| Marketplace | 3,033 | 2,261 | 2,023 | 2,506 | 4,487 |

| Other | — | — | — | — | 90 |

| Total premium revenue | 26,855 | 30,883 | 32,529 | 38,627 | 43,052 |

| Total premium revenue growth, derived | — | +15.0% | +5.3% | +18.7% | +11.5% |

Source: Form 10-K MD&A Segment Financial Performance — premium revenue by segment [5] [6] [7] [8]. Click any linked figure to open the filing page with the row highlighted.

Medical Margin by Program

| Medical Margin by Program | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Medicaid | 2,322 | 2,981 | 2,973 | 2,979 | 2,652 |

| Medicare | 430 | 437 | 388 | 603 | 475 |

| Marketplace | 399 | 290 | 499 | 617 | 423 |

| Other | — | — | — | — | 14 |

| Total medical margin | 3,151 | 3,708 | 3,860 | 4,199 | 3,564 |

Source: Form 10-K MD&A Segment Financial Performance — medical margin by segment [5] [6] [7] [8]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Income [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-17. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [9] [10] [11] [12]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows [13] [14] [15] [16]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income | Diluted earnings per share | Net cash from operating activities | Total stockholders' equity |

|---|---|---|---|---|---|---|

| FY2016 | 17,782 | 306 | 52 | 0.92 | 673 | 1,649 |

| FY2017 | 19,883 | (555) | (512) | (9.07) | 804 | 1,337 |

| FY2018 | 18,890 | 1,131 | 707 | 10.61 | (314) | 1,647 |

| FY2019 | 16,829 | 1,044 | 737 | 11.47 | 434 | 1,960 |

| FY2020 | 19,423 | 1,078 | 673 | 11.23 | 1,898 | 2,096 |

| FY2021 | 27,771 | 1,020 | 659 | 11.25 | 2,119 | 2,630 |

| FY2022 | 31,974 | 1,173 | 792 | 13.55 | 773 | 2,964 |

| FY2023 | 34,072 | 1,573 | 1,091 | 18.77 | 1,662 | 4,215 |

| FY2024 | 40,650 | 1,707 | 1,179 | 20.42 | 644 | 4,496 |

| FY2025 | 45,426 | 781 | 472 | 8.92 | (535) | 4,069 |

Source: consolidated statements across filings; older years from the standardized feed [13] [9] [1] [14]. Click any linked figure to open the filing page with the row highlighted.

Operating KPIs

| KPI | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Total membership | 5,199,000 | 5,258,000 | 4,995,000 | 5,535,000 | 5,491,000 |

| Medicaid membership | 4,329,000 | 4,754,000 | 4,542,000 | 4,890,000 | 4,568,000 |

| Marketplace membership | 728,000 | 348,000 | 281,000 | 403,000 | 655,000 |

| Consolidated medical care ratio (MCR) | 88.3% | 88.0% | 88.1% | 89.1% | 91.7% |

Source: company-reported operating metrics [5] [17] [6] [7]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-17. Estimate figures link to the consensus source, not to filing pages.

Traceability

306 of 336 figures on this page (91%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

All figures in US$ millions as printed in the filings, except per-share (US$) and ratio/percent rows. Fiscal year ends December 31.

Each FY2021–FY2025 column is cited to that year's own Form 10-K (income and cash flow statements print three years; balance sheets print two). Every core-statement cell in the FY2021–FY2025 columns is filing-verified.

Revenue breakdown and medical margin are the company's reported segments — Medicaid, Medicare, Marketplace and (from FY2024/FY2025) Other — taken from the MD A 'Segment Financial Performance' premium/medical-margin/MCR tables. The 'Other' segment premium is reported only from FY2025 ($90M); it was nil or not separately shown earlier.

Long-term record FY2016–FY2020 figures are from the standardized data feed (SEC XBRL) and are shown without page links; FY2021–FY2025 are filing-linked.

Quarterly Q4 FY25 income columns are derived (full-year FY2025 10-K less nine-month YTD from the Q3 FY2025 10-Q) and cross-check exactly to the quarterly data feed. Quarterly single-quarter operating cash flow is derived from printed year-to-date statements and also cross-checks to the feed.

1 figure(s) differed between the data feed and the filing; the filing value is shown (see the run's metrics/metrics_tab.json for the audit trail).

Molina Healthcare, Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Investor Day 2026 — 2026

Management's fullest and most current statement of the business — franchise, segments, growth engines, the margin dislocation and the path to the 2029 targets. · Open the full document →

Investor Day 2024 — 2024

The prior investor day — best for market size, competitive position and the unit-economics of the MCR advantage that the 2026 deck assumes. · Open the full document →

More from management

Investor Day 2023 — 2023 · 79 pages · The earlier edition of this narrative, and where management first set the 2026 premium and EPS targets it is now measured against. · Open →

Molina Healthcare, Inc.'s management answers for the business every quarter. These are the exchanges that explain it best — verbatim, from the call transcripts preserved in Sources. Each link opens the full transcript at that page in a new tab.

Q1 FY2026 Earnings Call — Q1 FY2026 (Apr 2026)

The current state of the recovery: how management splits trend from acuity, why it is holding guidance, the Medicare-to-duals rebuild, and its M&A math. · Open the full transcript →

Splits 2025's 7.5% Medicaid trend into a one-time redetermination acuity shift and the 5% core carried into 2026.

Joe Zubretsky, President & CEO: Last year, we observed a 7.5% medical cost trend that included 250 basis points of acuity shift related to the post-pandemic redetermination process. However, the acuity shift in core utilization impacts diminished as the year progressed. Our expectation that the acuity shift trend that we had experienced in 2025 was behind us and would not recur is holding up. We feel confident in our 5% medical cost trend assumption for 2026.

p. 1 · Read in context →

Asked why not raise guidance after a strong quarter, he explains the prudence and the loss-ratio cushion in the full-year number.

Joe Zubretsky, President & CEO (responding to Kevin Fischbeck, Bank of America): We use the term time tested because I think it is prudent to see 6 months of results before updating our guidance, particularly coming off a highly volatile medical cost inflection environment in 2025, bearing in mind in Medicaid with a 92% result in the first quarter a 92.9% indication in our guidance for the full year, we can actually produce loss ratios north of 93% and still hit our guidance for the rest of the year. So cautious perhaps, but in this environment, we think it's entirely prudent to do so.

p. 5 · Read in context →

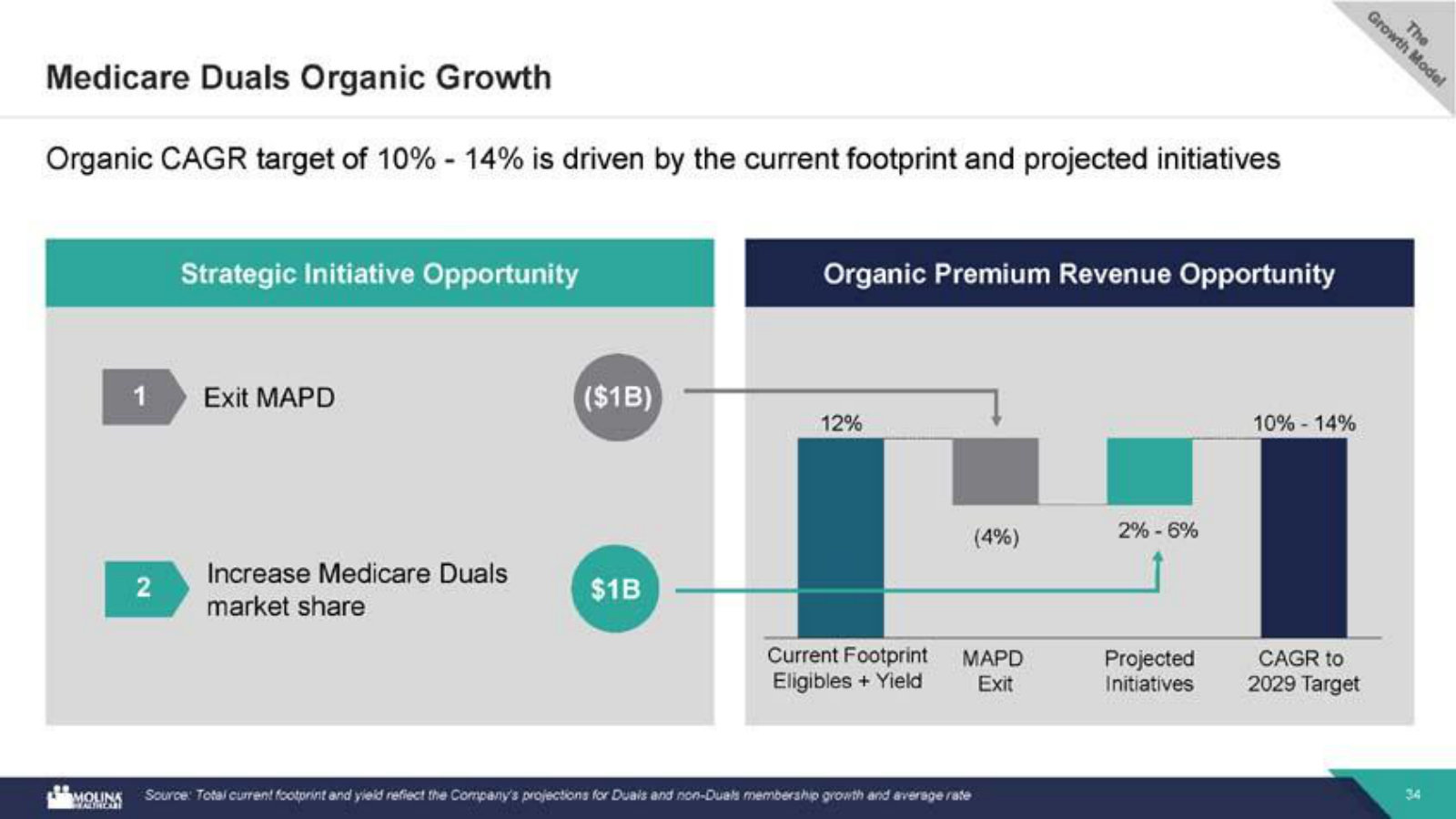

Lays out the Medicare rebuild — D-SNP, the MMP-to-HIDE/FIDE conversion, and the MAPD exit — into a pure duals business.

Scott Fidel (Goldman Sachs), analyst; Joe Zubretsky, President & CEO: You're right to point out that the Medicare story is a little more complicated than most because it's a combination of our D-SNP product, which has been in force for many years; our MMP members who have now converted to HIDE and FIDE; and our MAPD product, which we are going to eliminate for 2027. We cited a drag on this year's earnings due to the MAPD product — I think we said it produced about a $1 earnings per share drag that won't repeat next year — and it is tracking to plan. D-SNPs have always produced a modest profit and continue to.

p. 8 · Read in context →

M&A capital allocation: buying plans near book value can beat a new contract win when you're mostly paying for regulatory capital.

John Stansel (JPMorgan), analyst; Joe Zubretsky, President & CEO: Our M&A pipeline is full of actionable opportunities. We'll remain disciplined and focus on properties that fit our core strategy. Mark and I debate this often: historically we paid around 22 to 23 percent of revenue, but book value now seems the best benchmark. If you're only paying for regulatory capital, an M&A deal can be as good as, if not better than, a new contract win.

p. 9 · Read in context →

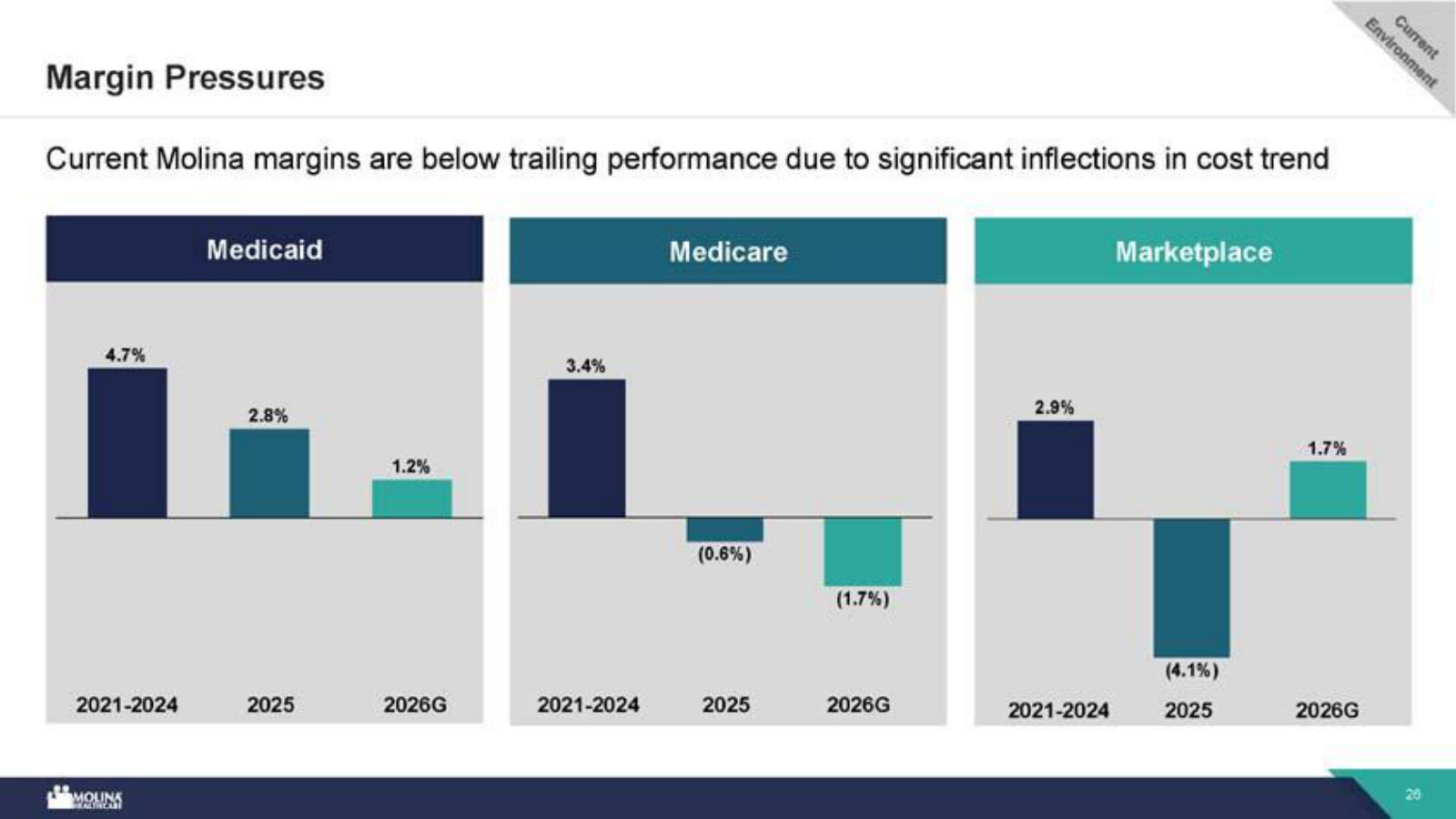

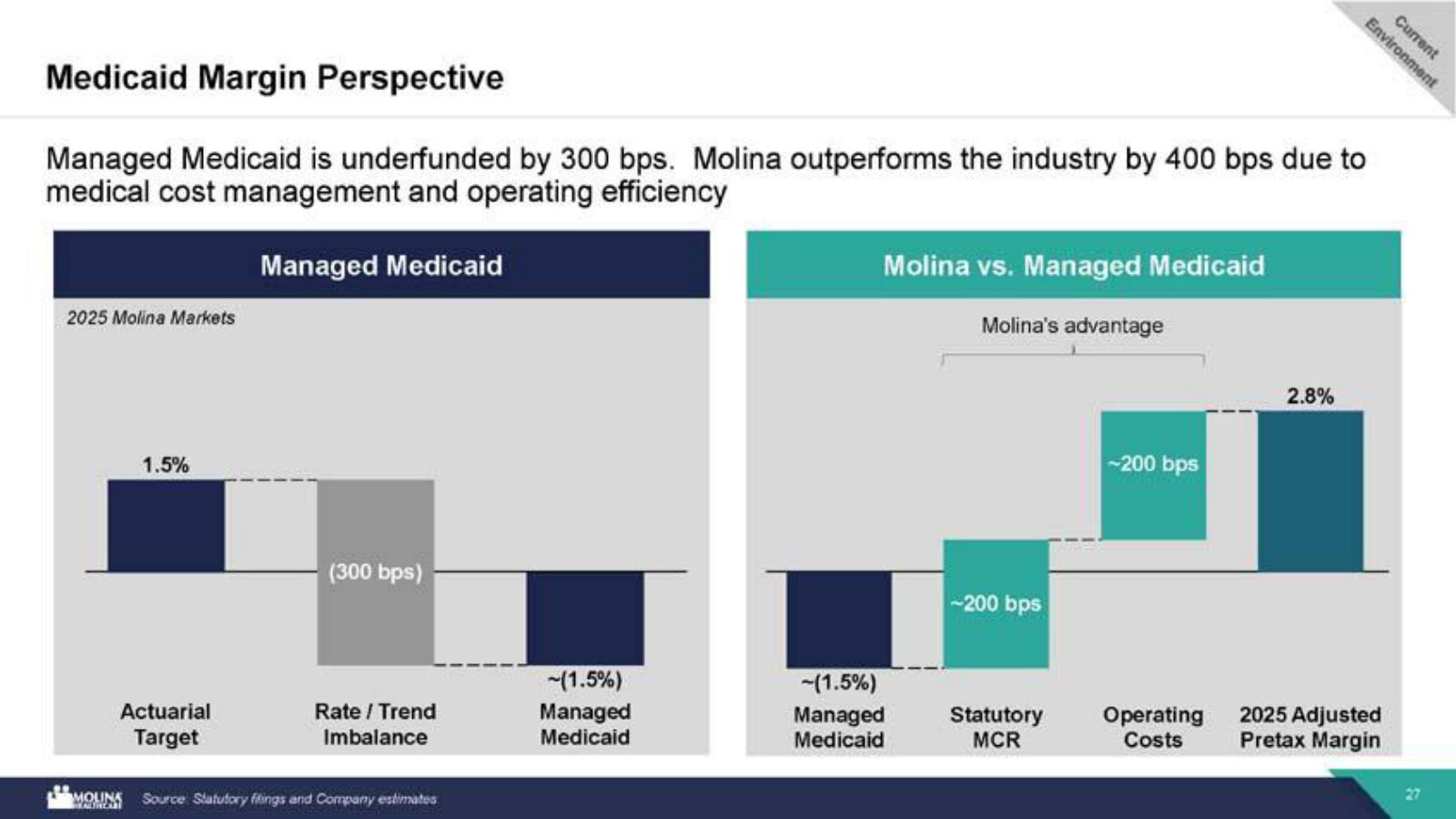

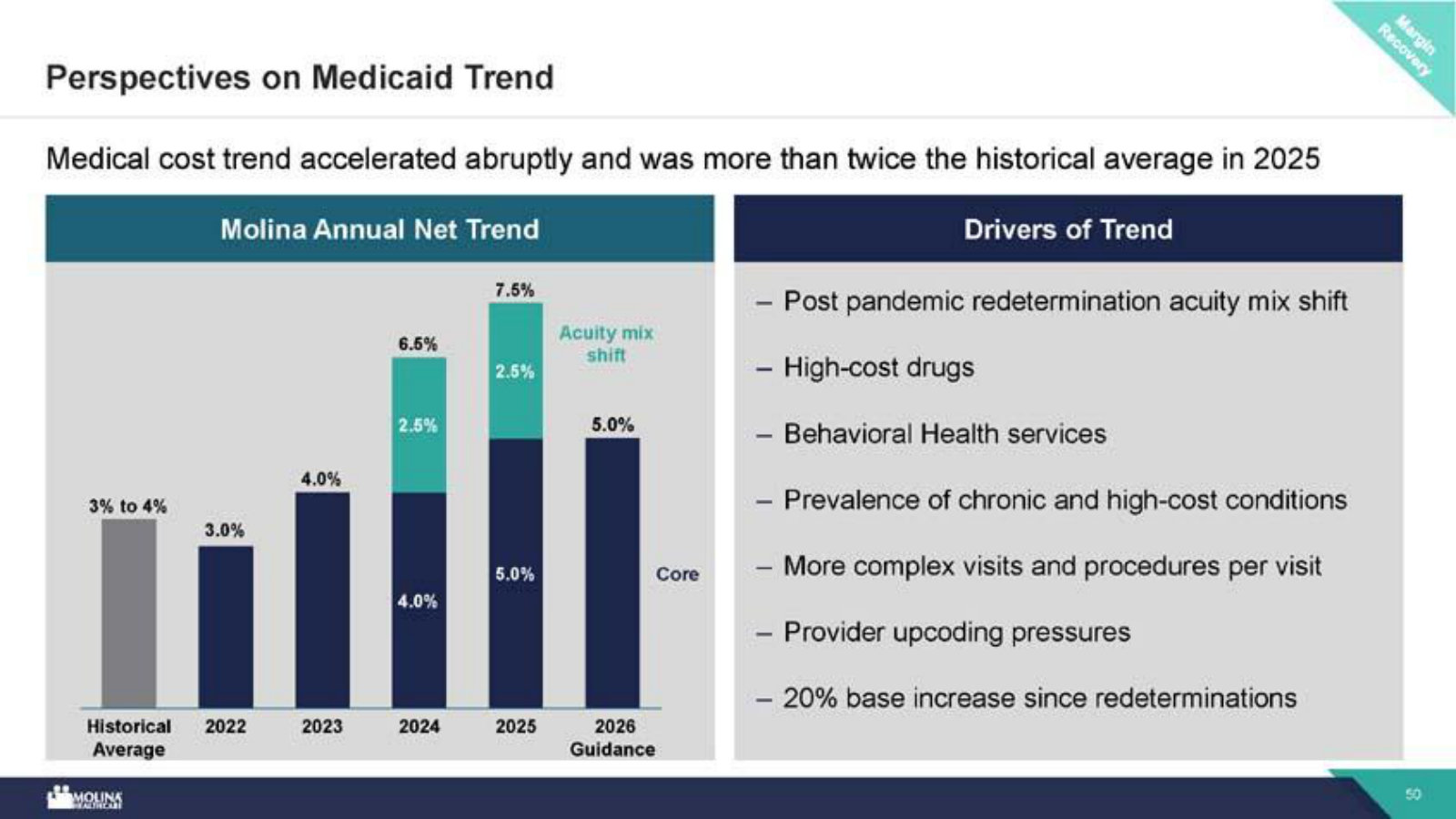

The recovery math: a cost base 20% above three years ago, states catching up on rates, Molina running 300-400 bps better than market.

Lance Wilkes (Bernstein), analyst; Joe Zubretsky, President & CEO: Generally speaking, we're seeing states step up to the reality that a cost inflection has occurred and they are catching up to it. What do they need to catch up to? If you look at the trends we've experienced over the past three years, 4.5, 6.5 and 7.5, the cost baseline is 20% higher than it was three years ago. That's what they need to catch up to. Now we believe we're operating 300 to 400 basis points better than the average market. So as they catch up, we should be moving into much more positive territory than we already are. Bearing in mind, our guidance in Medicaid is for a 1.5% pretax margin this year, eliminating the impact of Florida Kids.

p. 11 · Read in context →

Q4 & Full-Year 2025 Earnings Call — Q4 FY2025 (Feb 2026)

The reset: full-year attribution of a halved EPS, the anatomy of the Medicaid rate/trend gap, the growth engine, and the case that 2026 is the trough. · Open the full transcript →

Attributes the halving of EPS: Marketplace, at 10% of premium, drove nearly half the miss; Medicaid a third; Medicare the rest.

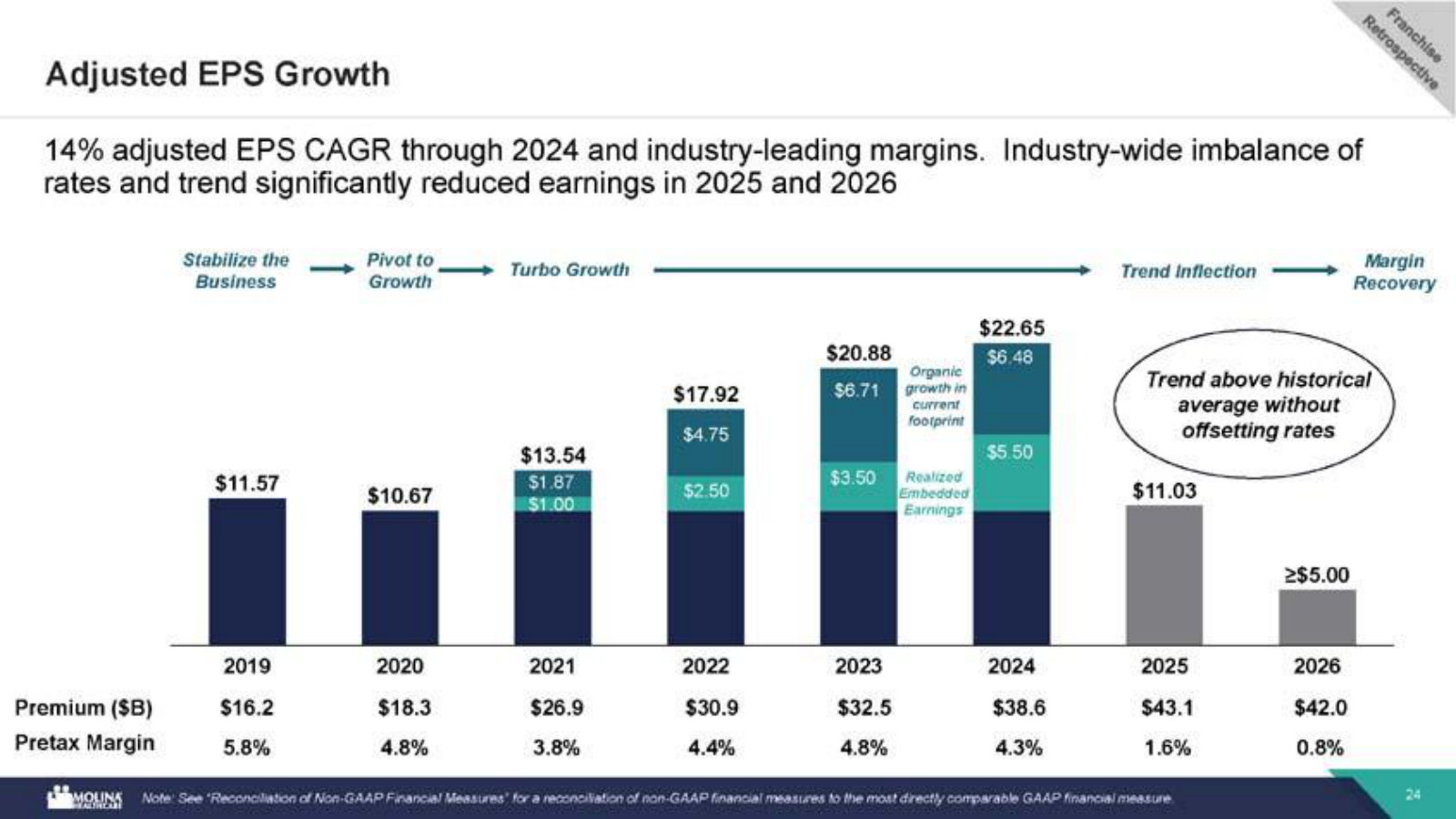

Joe Zubretsky, President & CEO: As we compare our initial 2025 EPS guidance of $24.50 to our final result of $11.03, nearly half of the underperformance for the year was attributable to the unprecedented trend and increased acuity in our Marketplace segment. A very disproportionate outcome given that the segment is just 10% of our total premium. The rate and trended balance in Medicaid accounted for approximately one-third of the underperformance, while the remainder was due to persistent higher utilization in Medicare.

p. 1 · Read in context →

The miss in one line: Medicaid rates rose to 6% while trend hit 7.5%, 250 bps of it the one-time redetermination acuity shift.

Joe Zubretsky, President & CEO: Rates increased from 4.5% in our initial guidance to 6% for the year, but medical cost trend continually increased from 4.5% in initial guidance to 7.5%, an unprecedented inflection in such a short period of time. 250 basis points of this 7.5% trend is attributable to the acuity shift from membership declines related to the final stages of redeterminations. While we are disappointed in our fourth quarter and full year results, many published reports indicate our Medicaid performance is industry-leading by 300 to 400 basis points in pretax margin.

p. 1 · Read in context →

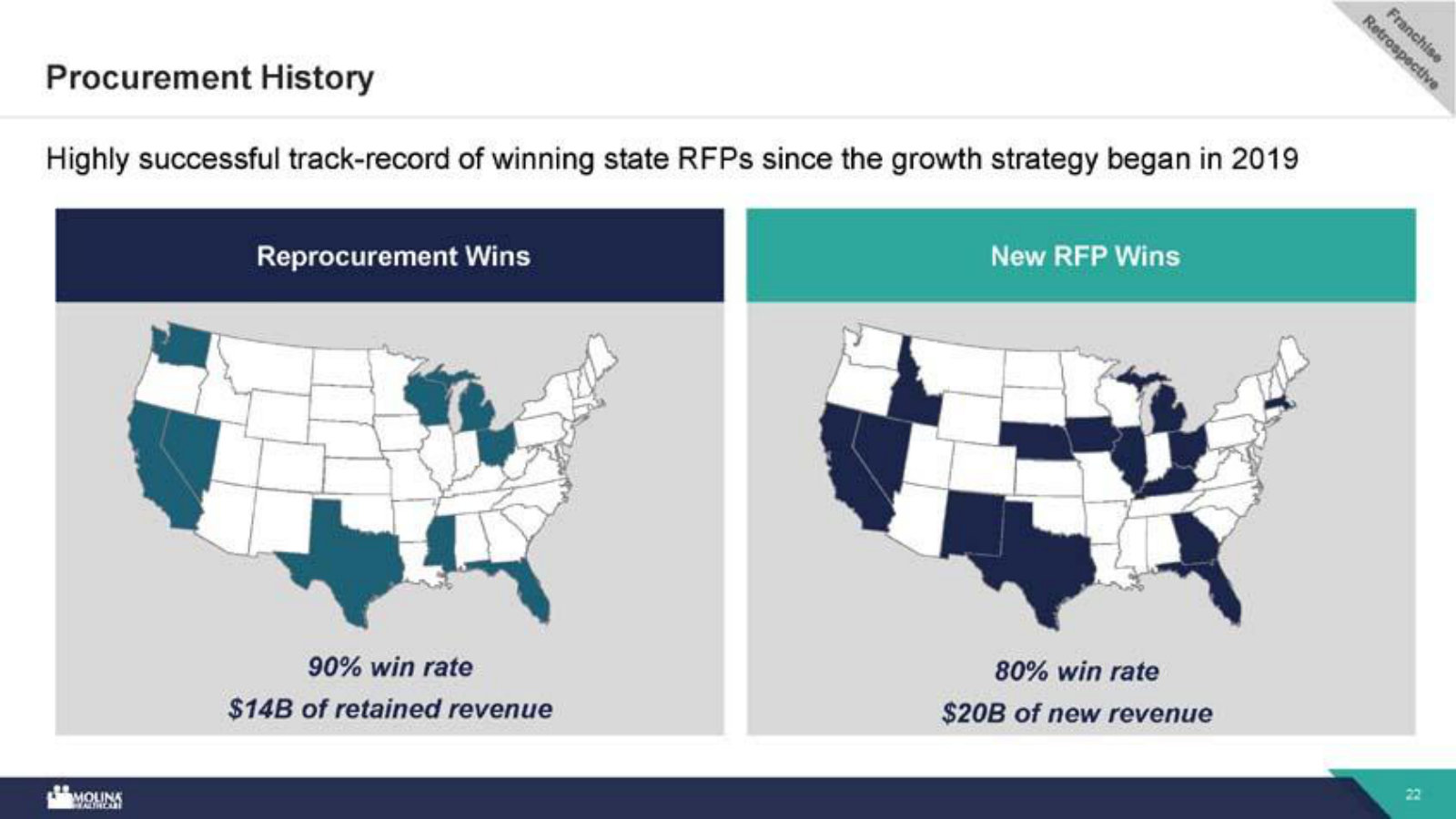

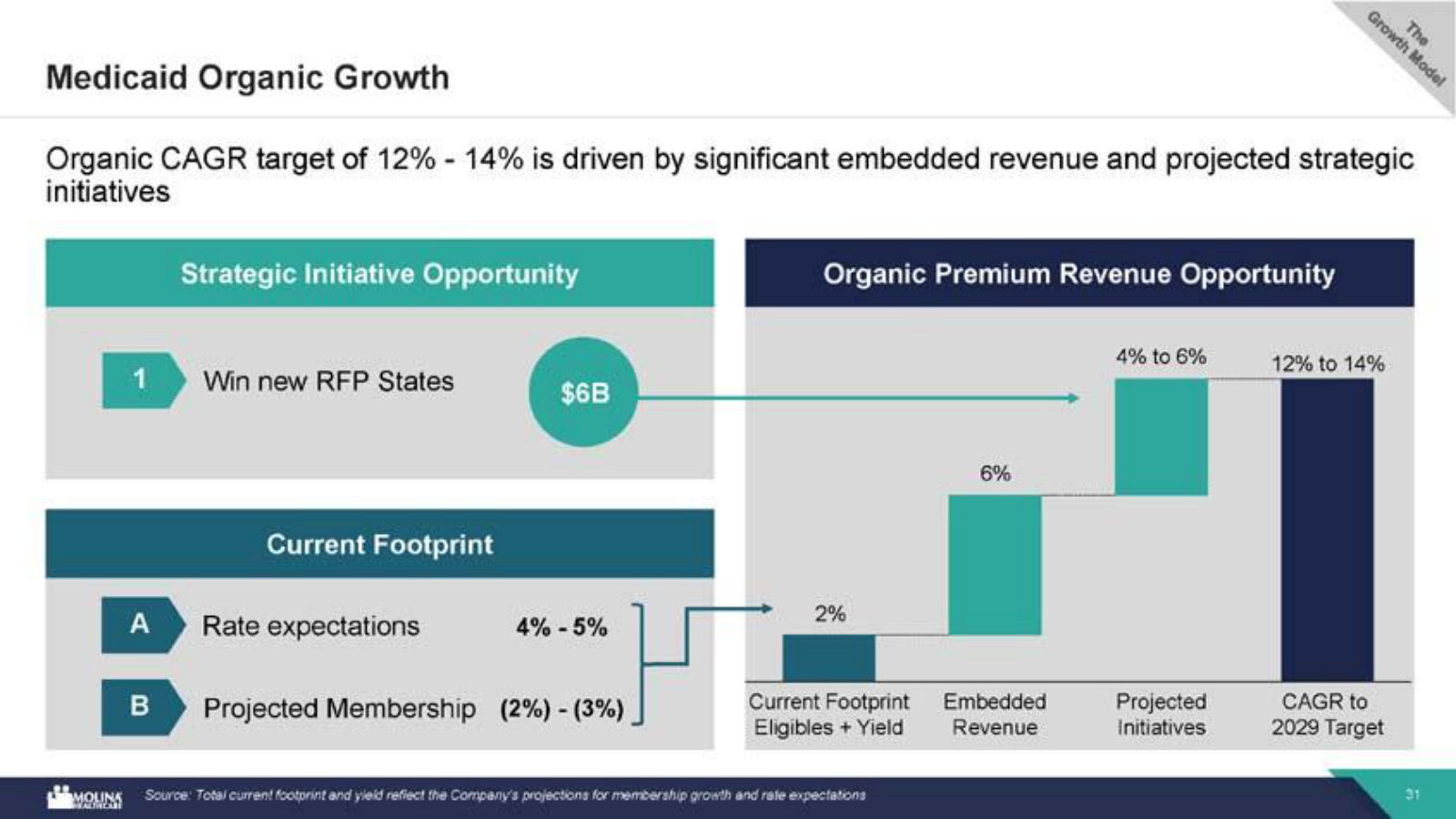

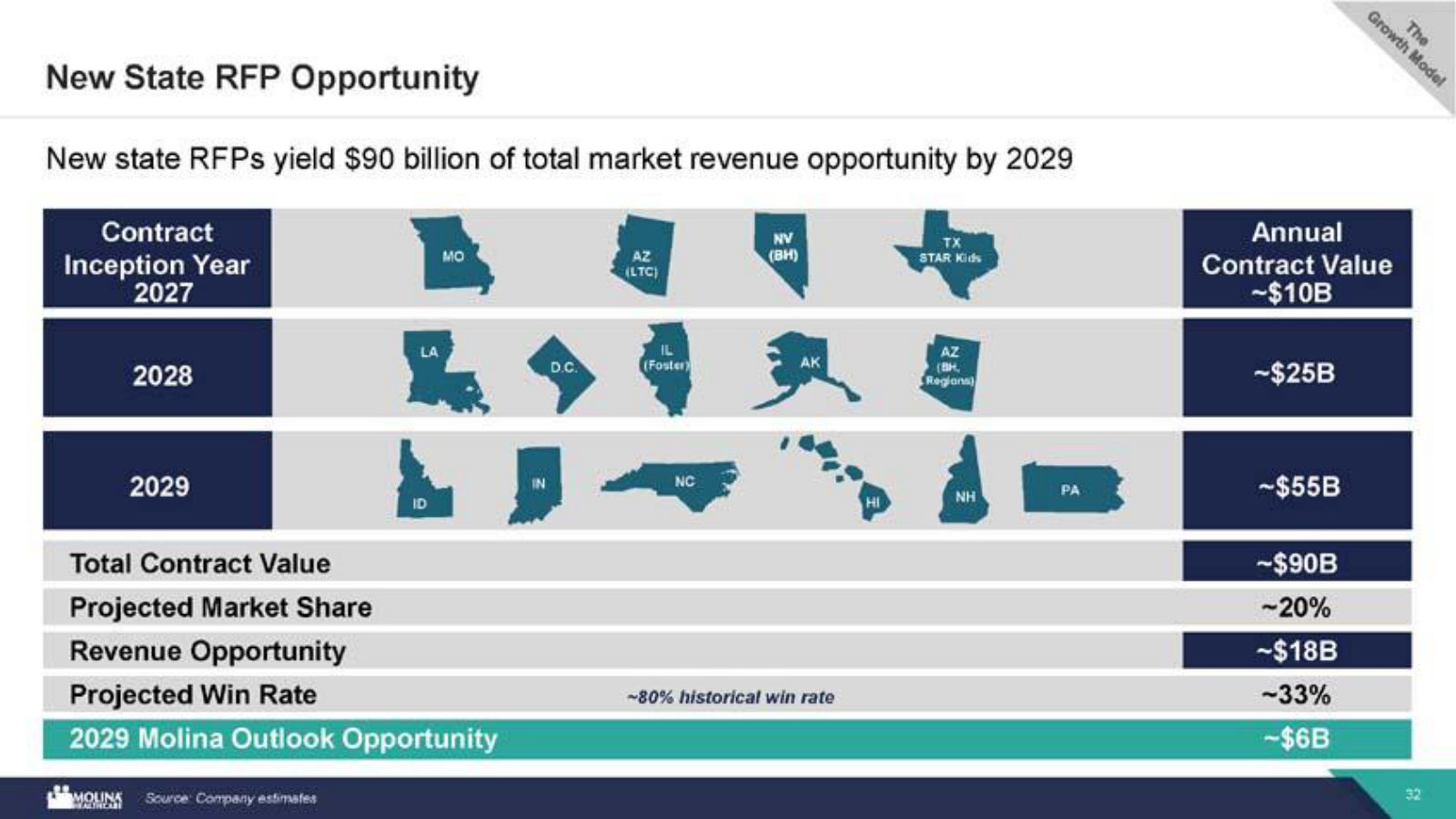

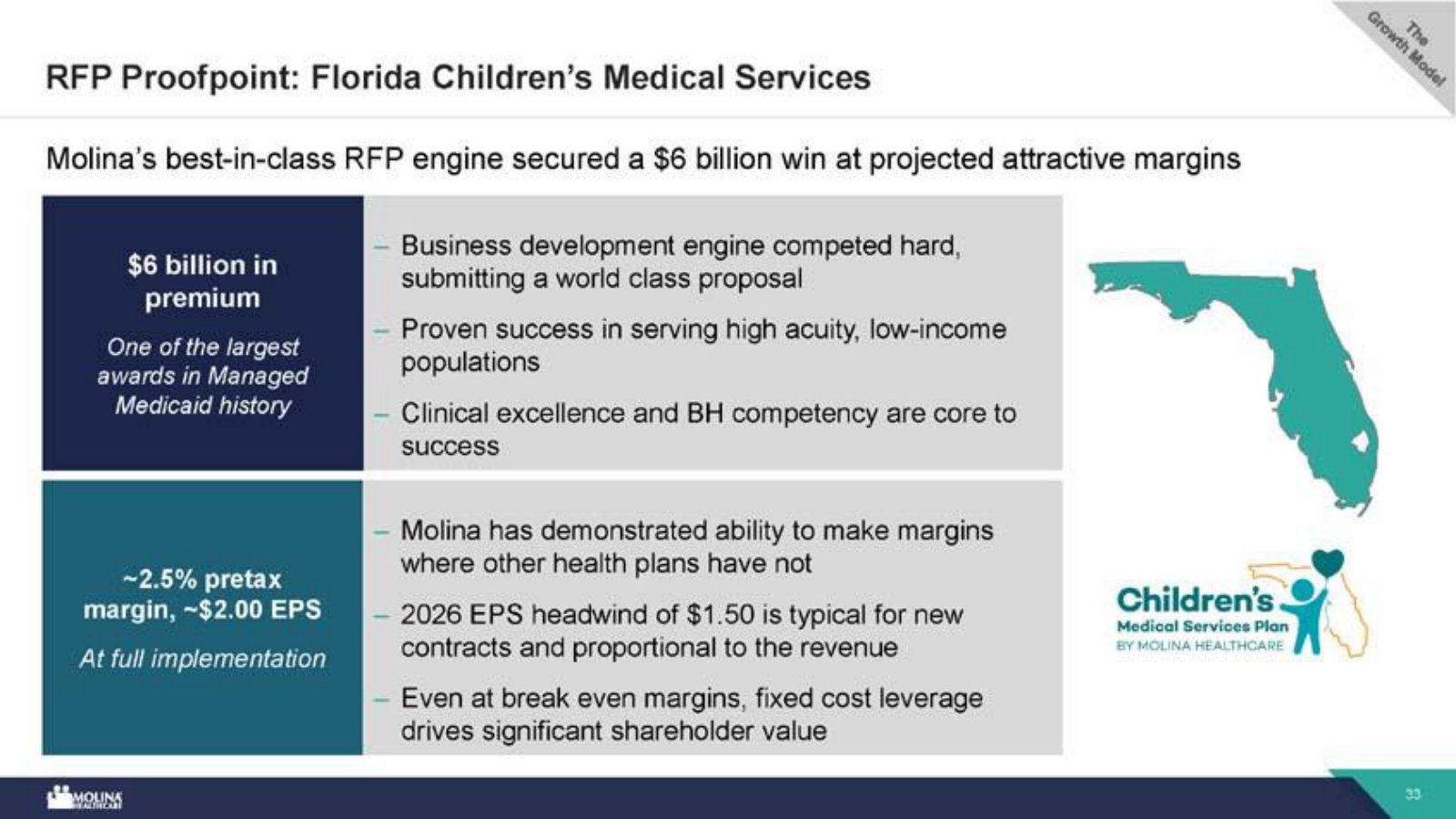

The growth engine still running in the downturn: 90%/80% RFP win rates, a $50B pipeline, and a historic $6B Florida CMS win.

Joe Zubretsky, President & CEO: During the quarter, Molina secured a historic RFP win in Florida where the state awarded Molina the sole Children's Medical Services or CMS contract. This contract is expected to yield $6 billion in annual run rate premium and is expected to go live in late 2026. […] Since we embarked on this growth strategy, we have achieved an RFP win rate of 90% on renewal contracts, representing $14 billion in retained revenue and 80% on new contracts representing $20 billion of new revenue. We are engaged in active RFPs in several states and have an active pipeline of $50 billion of new opportunities over the next few years.

p. 1 · Read in context →

The forward thesis: 2026 is the margin trough, the market lags 300-400 bps, and each 100 bps of Medicaid MCR is worth ~$5 of EPS.

Joe Zubretsky, President & CEO: We believe our 2026 forecast for Medicaid is the trough for managed Medicaid margins. In this margin trough, we expect that Molina Medicaid will produce a low single-digit margin, not losses, and that the market is underfunded by 300 to 400 basis points. We are confident in the outlook for this business and that rates and trend will eventually reach equilibrium. […] This potential is significant as every 100 basis points on the Medicaid MCR is worth nearly $5 per share. […] Embedded earnings are now greater than $11 per share.

p. 3 · Read in context →

Challenged that a 5% 2026 trend is too low after 7.5%, he strips out the 250 bps acuity shift and details the cost categories.

Ann Hynes (Mizuho), analyst; Joe Zubretsky, President & CEO: Therefore, when I see a 5% trend projected for the future, I find that insufficient. I would appreciate more detailed information regarding specific state actions, utilization management, or anything else that could clarify why you believe the trend will only grow by 5%. […] we had a 7.5% trend in '25 off of '24. With perfect hindsight, 2.5 percentage points of that was related to the redetermination related acuity shift as we've just been describing in a couple of questions that were asked. So core trend is 5%. Core trend includes every impact. It's a supply and demand economy. It includes the higher acuity of the American population that we serve. It includes any 'upcoding' or aggressive billing from providers. 5% is what we experienced in 2025. And again, it's off a cost base that's increased 20% over the past 3 years. It's 50% higher than historical averages. Medicaid trend over the last 10, 15 years has been 2% to 3%.

p. 9 · Read in context →

Q2 FY2025 Earnings Call — Q2 FY2025 (Jul 2025)

The shock: a $5.50 guidance cut mid-year. The thesis gets tested — what is driving costs, why the corridor hedge ran out, and whether rates can ever catch up. · Open the full transcript →

Catalogs the cost drivers of the shock — behavioral, high-cost drugs, inpatient, ER — and calls their persistence unprecedented.

Joe Zubretsky, President & CEO: Behavioral health costs have increased nationally reflecting both supply side and demand side drivers and imposed limitations on utilization management in certain states. High-cost drugs remain a source of pressure driven by higher script volumes and the introduction of a variety of expensive therapies beyond GLP-1s for conditions such as cancer and HIV. Higher inpatient utilization in the quarter was driven by a higher volume of admissions for complex health episodes, many of which originated from increased ER visits. […] This is the fourth consecutive quarter we have observed some combination of these trends. The magnitude and persistence of these medical cost increases are unprecedented.

p. 1 · Read in context →

The clearest teaching on the mechanism: how rates and risk corridors buffered trend, then were exhausted quarter by quarter.

Joe Zubretsky, President & CEO: Starting in the third quarter of 2024, while an increasing trend emerged from the end of the redetermination process, rates and Molina's risk corridor positions at the time were sufficient to offset that increasing trend. By the fourth quarter of 2024, the increasing medical cost trend moved beyond the 2024 midyear rate updates, and corridors have largely become depleted. Moving into the first quarter of 2025, the January 1 rate cycle captured much of the continued trend pressure. And now in the second quarter of 2025, we experienced yet another increase in trend, which moved beyond the rate updates received in the first quarter, and risk corridor protection at this point is very limited and isolated.

p. 2 · Read in context →

The cut, and the concentration lesson: Marketplace is 10% of revenue but nearly half the 140 bps of MCR pressure behind it.

Joe Zubretsky, President & CEO: Our full year 2025 adjusted earnings per share guidance is now expected to be no less than $19 per share, a floor, if you will, which is $5.50 below our initial guidance of $24.50 […] Our full year guidance now includes 140 basis points of consolidated MCR pressure compared to our initial guidance at $24.50, which is disproportionately attributed to Marketplace. Marketplace is 10% of our revenue and accounts for nearly half of this 140 basis point MCR revision.

p. 2 · Read in context →

Why Marketplace's natural hedge failed: a market-wide 8% jump in risk-pool acuity means risk adjustment can't keep up with trend.

Josh Raskin (Nephron Research), analyst; Joe Zubretsky, President & CEO: So I guess I'm just still struggling with what do you think is the root cause of this pickup in utilization and now, I guess, market-wide? […] The acuity of the entire marketplace risk pool is higher by 8% year-over-year, which means on a relative basis, risk adjustment is not going to keep up with the elevated trend. As I said, we've increased our trend assumption from 7% that went into pricing to 11% in our forecast.

p. 7 · Read in context →

The hardest question — if rates always lag a shifting risk pool, do you ever catch up? — answered with candid uncertainty on timing.

Kevin Fischbeck (Bank of America), analyst; Joe Zubretsky, President & CEO: you'll get the rate cycle to reflect last year's cost, but this year's cost will be high. This year's cost, we'll still see risk pool shifts. So like do you ever catch up? […] Currently, we are operating at a 91% medical cost ratio, which is 190 basis points above the upper limit of our range. To reach our target margin, we need an additional 200 basis points on top of the trend. Based on external evaluations, we believe that the wider market will require even more than this. If we can secure those extra 200 basis points along with an appropriate trend, we should be able to return to our target margin. Whether this will be achieved by January 1, 2026, is still uncertain.

p. 11 · Read in context →

Q4 & Full-Year 2024 Earnings Call — Q4 FY2024 (Feb 2025)

The pre-crisis annual: the growth algorithm, how risk corridors really work, Marketplace pricing calibration, and Medicaid's political durability. · Open the full transcript →

The growth algorithm in plain terms — new state wins — and why embedded earnings near 30% of run-rate EPS underwrite future growth.

Joe Zubretsky, CEO: 2024 was an extraordinary year for securing future growth on top of the reported 19% premium revenue growth, starting with recent acquisitions. […] in Georgia, the state announced its intent to award it to Medicaid managed care services contract. This was a significant win with an estimated $2 billion in annual premium revenue based on expected market share. […] Having embedded earnings of at least 20 to 25% of run rate EPS is an attractive benchmark to support future EPS growth. Now at approximately 30%, we are very well positioned to meet our long-term targets.

p. 2 · Read in context →

The best explanation of why risk corridors are an imperfect hedge: protection is uneven across 21 states, may miss where trend hits.

Andrew Mok (Barclays), analyst; Joe Zubretsky, CEO; Mark Keim, CFO: It's a matter of geography. As we've always said, we're almost loathed to give a number of how deep we are in corridors because while it is a hedge, it's an imperfect hedge. If you have underperformance, it depends where that underperformance happens, whether you get the benefit of the corridor. In the fourth quarter this year, while we had forecasted, I believe, 50 basis points of trend pressure absorbed by the corridors, it didn't pan out that way. […] We're in 21 states. And the benefit of the corridor is not evenly distributed across 21 states. So what really matters is where does the trend pressure show up versus where is corridor protection remaining. That could either help you significantly or it can leave you no benefit, which is more or less what happened in the fourth quarter.

p. 6 · Read in context →

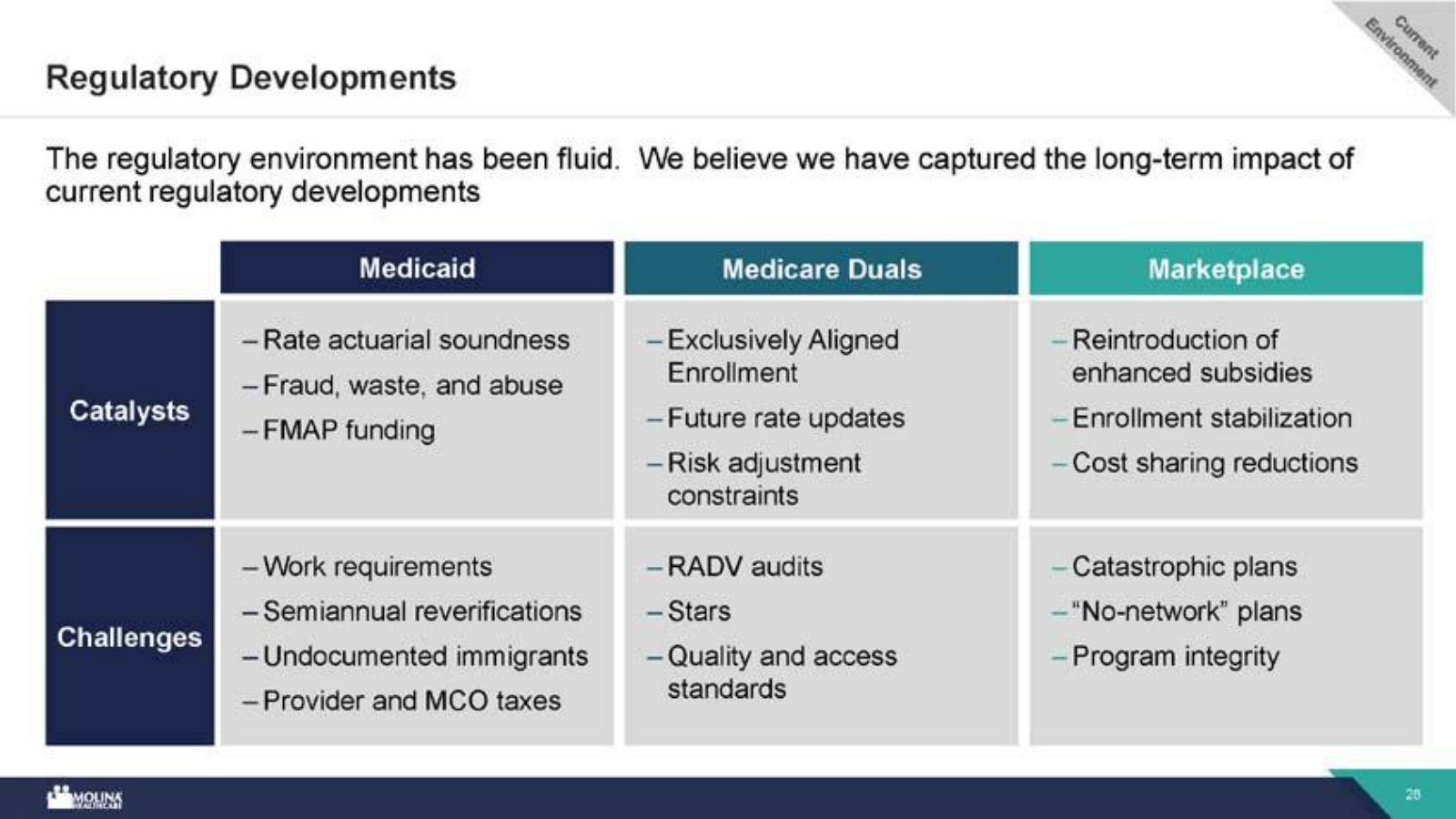

The political-durability thesis: whatever the funding mechanism, neither party wants more uninsured, so Medicaid change stays marginal.

A.J. Rice (UBS), analyst; Joe Zubretsky, CEO: the market really focuses on the how. You know, if you come up with a per capita cap scheme, FMA match for reduction FMAP match reduction on expansion, block match, whatever the mechanism is the CBO can score. That's not the issue. The issue is what are you going to reduce in terms of where the money goes? […] Neither side of the aisle wants to see more uninsured. It's below ten percent of eligibles for the first time in decades. Reduction in benefits. Reduction in enrollment, reduction in payments to providers, or none of the above. And I either have to, as a state, decrease my education budget or raise taxes. None of those solutions is politically tenable. That's why we conclude that any changes to manage Medicaid as we know it today would be marginal.

p. 11 · Read in context →

How Marketplace pricing is calibrated: reinvest excess margin into growth or hit the three-year minimum-MLR rebate.

Scott Fidel (Stephens), analyst; Joe Zubretsky, CEO: we consciously when you're producing ten percent to eleven percent pretax margins two years in a row, one, you gotta remain competitive. And two, if you keep it there, you're gonna run into the three-year minimum MLR. So it makes perfect sense to invest the excess margin and growth. It's a calibration. You try to set your product to be competitively positioned. As I said, we are number one or two silver priced in fifty percent of our geographies. We netted a hundred and thirty thousand members in open enrollment. Had, I think, two hundred fifty thousand ads and a hundred and thirty terms, which gave us a nice jumping-off point. So we have high confidence in the mid-single-digit margin.

p. 14 · Read in context →

More calls

Q3 FY2025 Earnings Call — Q3 FY2025 (Oct 2025) · 13 pages · The second cut of the year ($19 to $14). Go here for the Marketplace swing from +$3 to -$2 of EPS and how H2 Medicaid was annualized into the 2026 baseline. · Open →

Q1 FY2025 Earnings Call — Q1 FY2025 (Apr 2025) · 12 pages · The calm before the storm: guidance still $24.50. The clearest statement of the actuarial-soundness thesis and Molina running 200-300 bps better than the market. · Open →

Q3 FY2024 Earnings Call — Q3 FY2024 (Oct 2024) · 14 pages · Mid-unwinding: management calls Q3 the 'widest point' between rates and trend, details the corridor burn-down, and points to a 9% Q4 rate update as proof states respond. · Open →

Q2 FY2024 Earnings Call — Q2 FY2024 (Jul 2024) · 13 pages · Where the corridor-as-buffer thesis was first stress-tested — the '200 basis points deep' concept defined, and Fischbeck pressing on why Molina saw less pressure than peers. · Open →

Q4 & Full-Year 2023 Earnings Call — Q4 FY2023 (Feb 2024) · 13 pages · The foundational annual: the plainest statement of the capitated-risk model, the growth track record ($12B reprocured, $7B new since 2019), and Bright acquisition accounting. · Open →

Q3 FY2023 Earnings Call — Q3 FY2023 (Oct 2023) · 12 pages · Redetermination mechanics as they unfolded: procedural vs. verification disenrollments, ~30% reconnect rate, and the Medicare cost drivers that led to 2024 benefit-design cuts. · Open →

Q2 FY2023 Earnings Call — Q2 FY2023 (Jul 2023) · 15 pages · The launch of Medicaid redeterminations explained from the ground up — ex parte renewals, retroactive reconnection, and the bottoms-up 2024 revenue bridge. · Open →

Molina Healthcare, Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Molina Healthcare, Inc. — FY2025 Annual Report (Form 10-K) — FY2025

The year the thesis was tested: net income fell to $472M from $1,179M as the medical care ratio jumped to 91.7%; OBBBA reshapes the runway. · Open the full document →

Item 1. Business — Overview — p. 7 · Read the full section →

Defines a pure-play government-sponsored insurer: ~5.5M members across 21 states, paid fixed premiums under four segments.

Item 1. Business — Trends and Uncertainties: OBBBA — p. 23 · Read the full section →

Management's own read on the legislative shocks that shrink the runway — Medicaid work rules and expiring Marketplace subsidies.

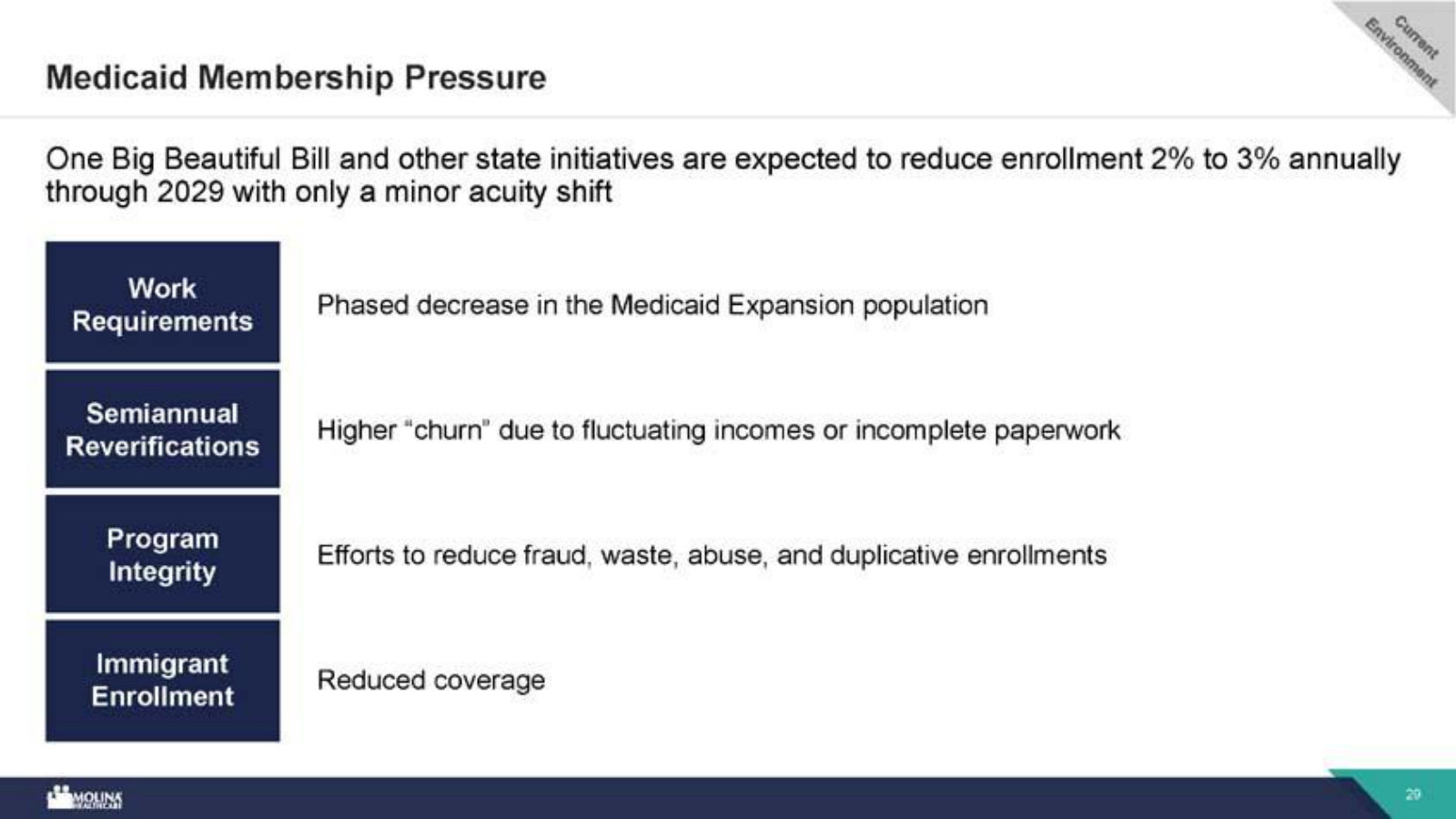

OBBBA's expected 15–20% cut to 1.2M Expansion members and phased Marketplace eligibility curbs.

The President signed the OBBBA into law in July 2025, which contains changes to the Medicaid and Marketplace programs. […] We currently estimate the reduction in enrollment will be in the range of 15% to 20% by 2029 on 1.2 million members in our Medicaid Expansion population, and any acuity shifts should be modest and gradual. […] The law limits which legal aliens may be eligible for Marketplace PTCs and will require pre-enrollment eligibility verification for enrollees to receive PTCs. These changes are planned to be phased in over the period from 2026 to 2028 and are expected to reduce national Marketplace enrollment as well.

p. 23 · Read in context →

Item 1A. Risk Factors — p. 39 · Read the full section →

The two risks that actually bite a thin-margin capitated insurer: state rates lagging cost trend, and a volatile Marketplace.

Fixed premiums vs rising costs — the core margin risk, already showing up in prior quarters.

Our premium revenues consist of fixed monthly payments per member, and supplemental payments for other services such as maternity deliveries. These premiums are fixed by contract, and we are obligated during the contract periods to provide healthcare services as established by the state governments in which our health plans operate. […] If the premiums paid to us are not increased at a rate that is commensurate with the rate at which medical expenses related to healthcare services rise, or the rate at which health care utilization rates increase, our medical margins will be compressed or eliminated, and our earnings will be negatively affected. We have seen in prior quarters that medical expenses have risen higher than anticipated, and that our capitation rates have not kept pace with the sharp rate of that medical care cost increase.

p. 39 · Read in context →

Margin fragility quantified: one point of MCR would have cut diluted EPS from $8.92 to ~$2.72.

Because the premium payments we receive are generally fixed in advance and we operate with a narrow profit margin, relatively small changes in our medical care ratio can create significant changes in our overall financial results. For example, if our overall medical care ratio of 91.7% for the year ended December 31, 2025, had been one percentage point higher, or 92.7%, our net income per diluted share for the yea ended December 31, 2025 would have been approximately $2.72 rather than our actual net income per diluted share of $8.92, a difference of $6.20.

p. 41 · Read in context →

Item 7. MD&A — Consolidated Results — p. 77 · Read the full section →

Management explains why 2025 earnings halved: MCR rose across every segment while rates lagged.

The earnings decline attributed to higher MCR across all segments and interest expense.

The decline in net income in 2025 reflects a decline in operating income, which totaled $781 million in 2025, compared with $1,707 million in 2024. The decrease in operating income was mainly attributable to an increase in the MCR across all our segments, higher interest expense and lower investment income, partially offset by the benefit of higher premium revenues, and G&A expense efficiencies.

p. 78 · Read in context →

Item 7. MD&A — Segment Financial Performance — p. 81 · Read the full section →

Where the margin broke, segment by segment — Medicaid MCR to 91.8% and Marketplace normalizing off a 75.4% base.

Medicaid MCR up 150bps on utilization; rates lagging trend in a 'temporary' imbalance.

The Medicaid MCR increased 150 basis points to 91.8% in 2025, compared to 90.3% in 2024. The increase was driven by higher medical trend from an increase in utilization among our continuing population that was higher than we expected, and changes in member acuity and product mix. […] The increases to the MCR were partially offset by premium rate increases, but the rate increases have lagged the increase in medical cost trend, resulting in a rate and trend imbalance that we believe to be temporary.

p. 82 · Read in context →

Item 7. MD&A — Critical Accounting Estimates: Medical Claims and Benefits Payable — p. 94 · Read the full section →

The one estimate that defines a capitated insurer's earnings — IBNP reserves built on completion factors and cost-trend assumptions.

Why IBNP is the critical judgment: completion factors and healthcare cost trend drive the reserve.

The estimation of the IBNP liability requires considerable judgment in applying actuarial methods, determining the appropriate assumptions, and considering numerous factors. Of those factors, we consider estimated completion factors (measures the cumulative percentage of claims expense that will ultimately be paid for a given month of service based on historical payment patterns) and the assumed healthcare cost trend (percent change in per-member per-month incurred medical care costs) to be the most critical assumptions.

p. 94 · Read in context →

More annual reports

Molina Healthcare, Inc. — FY2024 Annual Report (Form 10-K) — FY2024 · 155 pages · The peak-margin baseline (MCR 89.1%, EPS $20.42) against which the FY2025 compression reads. · Open →

Molina Healthcare, Inc. — FY2023 Annual Report (Form 10-K) — FY2023 · 151 pages · Captures the Medicaid redetermination unwind as pandemic continuous-enrollment protections lapsed. · Open →

Molina Healthcare, Inc. — FY2022 Annual Report (Form 10-K) — FY2022 · 142 pages · Peak-enrollment year still boosted by pandemic-era continuous Medicaid coverage. · Open →

Molina Healthcare, Inc. — FY2021 Annual Report (Form 10-K) — FY2021 · 142 pages · The acquisition-fueled growth phase (Magellan Complete Care, Affinity) that built the current footprint. · Open →

Competitors describe Molina Healthcare, Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Centene Corporation (CNC)

Centene is Molina's closest pure-play peer — the largest Medicaid and ACA Marketplace insurer in the country, competing directly for the same state contracts, exchange members and dual-eligible populations.

Centene's 10-K claims the number-one position in Medicaid and Marketplace and one of the highest D-SNP concentrations among peers — the three government programs that make up Molina's entire book.

we are the nation's largest Medicaid and Marketplace insurer, as well as the largest stand-alone PDP provider. Our Medicare Advantage business includes one of the highest concentrations of D-SNP members among our peers, aligned with our focus on low-income, complex populations.

p. 12 · Read in context →

Centene sizes the Medicaid market (CMS: 7% annual growth to $1.5 trillion by 2031) and states its own Medicaid scale — 12.5 million members across 30 states.

CMS estimates Medicaid spending will grow at an average annual rate of 7% to $1.5 trillion by 2031. […] We are the largest Medicaid health insurer in the country, serving 12.5 million Medicaid members in 30 states as of December 31, 2025.

p. 14 · Read in context →

Centene's stated Marketplace scale — 5.5 million ACA exchange members in 29 states under its Ambetter brand — the same subsidized-individual market where Molina competes.

We are the largest Marketplace carrier, serving 5.5 million members across 29 states as of December 31, 2025, under the brand name Ambetter Health.

p. 18 · Read in context →

Elevance Health, Inc. (ELV)

Elevance is one of the largest Medicaid managed-care operators and a major ACA carrier; its earnings calls detail the Medicaid rate/acuity squeeze and Medicaid-to-exchange migration that also drive Molina's results.

Elevance's CFO says state Medicaid rates continue to lag member acuity, pushing its 2025 Medicaid margin modestly negative with a further decline of at least 125 bps expected in 2026 — the rate-adequacy squeeze common to Medicaid MCOs.

Mark Kaye (CFO): Medicaid performance reflected pressure from elevated acuity and utilization, which were not fully offset by rate updates. We now expect our full year 2025 Medicaid operating margin to be modestly negative, establishing a baseline from which we anticipate a decline of at least 125 basis points in 2026 as rates continue to lag acuity and utilization trends remain elevated.

p. 2 · Read in context →

Elevance's CFO attributes roughly 70% of its rising ACA medical-cost trend to higher-acuity members moving from Medicaid into the exchanges during redeterminations — a market-migration dynamic that runs across Molina's Medicaid and Marketplace lines.

Mark Bradley Kaye (CFO): There are three main factors we are observing that contribute to the significant increase in medical trends in our ACA business. First, the risk pool's acuity and morbidity have significantly increased due to a higher ratio of healthier members, particularly in states with a larger number of fully subsidized individuals. This change has been driven by market exits and the movement of higher acuity members from Medicaid to ACA during the redetermination process, which accounts for approximately 70% of the total impact.

p. 3 · Read in context →

Elevance ties its 2026 Medicaid membership outlook to redetermination normalization, state program changes and RFP outcomes — naming competitive state contract results as a swing factor in the shared Medicaid market.

Mark Kaye (CFO): our Medicaid membership outlook, while very preliminary at this point, does consider things like the continued normalization following the redetermination process as well as the impact of state program changes and RFP outcomes. Whilst we do expect some churn to persist into next year, we do expect the pace of disenrollment to be manageable, and we are beginning to see stabilization in some of our markets.

p. 10 · Read in context →

UnitedHealth Group Incorporated (UNH)

UnitedHealth's Community & State unit is among the largest Medicaid managed-care businesses; through it and its D-SNP/duals franchise, UNH bids against Molina for state Medicaid contracts.

UnitedHealth sizes its Medicaid franchise (UnitedHealthcare Community & State) at more than 7.4 million people across 33 states and DC, including 1.2 million in ACA Medicaid expansion — the scale a state-focused rival like Molina competes against.

UnitedHealthcare Community & State’s primary customers oversee Medicaid plans, including Temporary Assistance to Needy Families; Children’s Health Insurance Programs (CHIP); Dual SNPs (DSNPs); Long-Term Services and Supports (LTSS); Aged, Blind and Disabled; and other federal, state and community health care programs. As of December 31, 2024, UnitedHealthcare Community & State participated in programs in 33 states and the District of Columbia, and served more than 7.4 million people; including 1.2 million people through Medicaid expansion programs in 20 states under the Patient Protection and Affordable Care Act (ACA).

p. 12 · Read in context →

UnitedHealth's UnitedHealthcare president cites state-rate pressure, expected Medicaid membership attrition and negative 2026 margins pending state rate alignment — the same Medicaid funding backdrop Molina navigates.

Timothy Noel (President, UnitedHealthcare): Community & State results continue to reflect pressures in state-based rate environments, but were within the overall expected range. […] In Medicaid, we remain focused on improvements in high acuity care management and operating cost management. […] We continue to expect membership attrition and negative margins in 2026 in light of continuing high trend and insufficient funding with modest margin improvements beginning in 2027. […] Appropriately aligning state rates to elevated medical cost trends in these programs is essential to sustainably serving people who rely on them.

p. 2 · Read in context →

CVS Health Corporation (CVS)

Through Aetna, CVS competes in Medicaid, Medicare Advantage, D-SNP and duals — though it exited the ACA exchanges in 2026, marking a strategic divergence from Molina's exchange growth.

CVS's CFO frames the individual-exchange exit as a 2026 tailwind and takes a 'cautious outlook' on Medicaid amid industry-wide pressure — Aetna prioritizing margin over the exchange and Medicaid growth Molina pursues.

Brian Newman (Chief Financial Officer): This includes another year of progress in our Medicare Advantage business, supported by our disciplined approach to plan design and footprint in individual as well as repricing opportunities in our group business. We also expect a tailwind from our exit of the individual exchange business. Although our conversations with our Medicaid state partners continue to progress and this business has performed in line with our expectations this year, we are taking a cautious outlook in light of the broader pressures across the industry.

p. 5 · Read in context →

Humana Inc. (HUM)

Humana is Medicare-centric but is expanding its Medicaid footprint (now 13 states, adding Georgia and Texas) and is a large dual-eligible/D-SNP player, overlapping Molina in duals and state Medicaid.

Humana lists its Medicaid state-contract footprint (10 states) and its dual-eligible integration strategy across Medicaid, Medicare Advantage and PDP — the duals and Medicaid ground where the Medicare-centric insurer overlaps Molina.

We have contracts in multiple states to serve Medicaid-eligible members, including Florida, Kentucky, Illinois, Indiana, Louisiana, Ohio, Oklahoma, South Carolina, Virginia and Wisconsin. We also serve members who qualify for both Medicaid and Medicare, referred to as "dual eligible", through our Medicaid, Medicare Advantage, and stand-alone prescription drug plans. As the dual eligible population represents a disproportionate share of costs, Humana is participating in varied integration models designed to improve health outcomes and reduce avoidable costs.

p. 10 · Read in context →

Humana's CEO says its Medicaid footprint now spans 13 states, with Georgia and Texas launching next year — a direct expansion into large Medicaid markets where Molina operates.

James Rechtin (President and CEO): we continue to grow our Medicaid and CenterWell footprint. Medicaid now spans 13 states. Including Georgia and Texas, which are anticipated to launch next year. We also hope to soon announce a strategic acquisition in the primary care space.

p. 2 · Read in context →

Humana's Medicaid (state-based) membership grew 10.7% to about 1.6 million as of year-end 2025, driven mainly by its newly implemented Virginia contract — evidence of a peer adding Medicaid share through state wins.

State-based contracts and other membership increased 155,700 members, or 10.7%, from 1,459,900 members as of December 31, 2024 to 1,615,600 members as of December 31, 2025 primarily due to the Virginia contract implemented in 2025 […]

p. 50 · Read in context →

The Cigna Group (CI)

Cigna is the most distant peer: it has no Medicaid or Medicare risk business and has deliberately shrunk its ACA exchange book, so it collides with Molina only at the individual-exchange edge.

Cigna's president states it has 'no exposure to Medicaid or Medicare,' serving those customers only through its Evernorth (PBM/services) portfolio — the clearest marker of how little Cigna's risk-bearing book overlaps Molina's.

Brian C. Evanko (President and COO): we have intentionally positioned our Cigna Healthcare portfolio with a product mix that has proven favorable in the current environment as we have no exposure to Medicaid or Medicare, instead choosing to serve these customers through our Evernorth services portfolio.

p. 3 · Read in context →

Cigna's president recounts shrinking its individual-exchange book from ~1 million to under 400,000 members to prioritize margin, noting competitors grew and industry exchange enrollment rose nearly 50% — sizing the ACA market Molina and Centene expanded into.

Brian C. Evanko (President and COO): At that point in time, we served nearly 1 million customers in the individual exchanges, albeit with mixed financial performance. Based upon our performance as well as our forward view of the market, we made the strategic choice to prioritize margin over growth, which included adjustments to product and network strategies, refinements to our geographic footprint, and increased prices where necessary. […] we now serve fewer than 400,000 customers in this business, down materially from the nearly 1 million we served in 2023. […] some of our competitors showed meaningful growth in their individual exchange businesses, while we chose to reposition our portfolio, which resulted in fewer individual exchange customers for Cigna Healthcare. […] Meanwhile, across the industry, individual exchange enrollment is up nearly 50% over that same time period.

p. 8 · Read in context →

More peer documents

Centene — Q1 FY2026 earnings call — Q1 FY2026 · 13 pages · Centene's CFO adds $1B of premium revenue 'largely driven by Texas Medicaid' and guides Marketplace membership down to ~3.5M after the enhanced-APTC expiration — a live read on the Medicaid RFP and exchange markets Molina shares. · Open →

Centene — Q4 FY2025 earnings call — Q4 FY2025 · 14 pages · Details the 2026 Marketplace revenue cliff (~-$8B) from APTC expiration and Medicaid member-months down 5-6% — quantifying the enrollment shock across both of Molina's largest lines. · Open →

Humana — FY2024 annual report (10-K) — FY2024 · 157 pages · Prior-year Medicaid state-contract list (9 states) and D-SNP membership of 937,100 — the baseline against which Humana's 2025 Medicaid/duals expansion is measured. · Open →

CVS Health — FY2024 annual report (10-K) — FY2024 · 340 pages · Enumerates Aetna's Public Exchange, Medicare Advantage, Medicaid, dual-eligible and D-SNP product regulation — a full map of where CVS/Aetna overlaps Molina before the 2026 exchange exit. · Open →

The Cigna Group — FY2024 annual report (10-K) — FY2024 · 214 pages · Describes Cigna's small ACA Individual & Family Plans (11 states) and notes Medicaid-redetermination members seeking marketplace coverage — the thin edge where Cigna touches Molina's world. · Open →

UnitedHealth Group — Q4 FY2025 earnings call — Q4 FY2025 · 13 pages · CFO Wayne DeVeydt quantifies 2026 Medicaid rate increases of 6-7% 'below our expectations' with expected margin and membership contraction — UNH's own read on Medicaid rate adequacy. · Open →

Source: S&P Capital IQ consensus via Xpressfeed · Generated 2026-07-17.

Street snapshot

The 17 price targets span a wide $129 to $286, with a $210.76 mean sitting just above the $209 median.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst counts shown explicitly; recommendation respondents: 19.

| Street view | Reading | Analysts |

|---|---|---|

| Recommendation mix | Buy 3, Outperform 0, Hold 15, Underperform 1, Sell 0 | 19 |

| Consensus score | 2.74 | 19 |

| Target price | mean 210.8; high 286.0; low 129.0 | 17 |

Forward table

The larger move is in earnings, where normalized EPS is modeled to more than halve to roughly $5.16 in FY2026 and then rebuild to $9.29 in FY2027, with no dividend forecast across the window.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst count is the estimate count for each period and metric.

| Period | Metric | Mean | YoY | Analysts | Low / high |

|---|---|---|---|---|---|

| FY0E | Revenue | 44,277 | -2.5% | 15 | 42,247 / 45,764 |

| FY0E | EBITDA | 682.8 | -33.8% | 9 | 552.4 / 749.0 |

| FY0E | EBIT | 535.0 | -50.8% | — | — / — |

| FY0E | Net income (GAAP) | 153.8 | -67.4% | 9 | 72.07 / 238.5 |

| FY0E | Net income (normalized) | 262.5 | -64.5% | — | — / — |

| FY0E | EPS (GAAP) | 3.32 | -62.7% | 7 | 1.41 / 4.66 |

| FY0E | EPS (normalized) | 5.16 | -53.2% | 19 | 4.36 / 5.60 |

| FY0E | Free cash flow | 1,861 | -433.5% | — | — / — |

| FY0E | Dividend per share | 0.00 | — | — | — / — |

| FY0E | Gross margin | 12.4% | -4.9% | — | — / — |

| FY0E | Capital expenditure | -129.7 | -4.6% | — | — / — |

| FY0E | Net debt | -1,315 | 56.6% | — | — / — |

| FY0E | ROE | 6.0% | -63.4% | — | — / — |

| FY0E | Cash from operations | 1,046 | -529.5% | — | — / — |

| FY+1E | Revenue | 47,524 | 7.3% | 14 | 44,242 / 50,874 |

| FY+1E | EBITDA | 964.2 | 41.2% | 9 | 762.1 / 1,179 |

| FY+1E | EBIT | 848.6 | 58.6% | — | — / — |

| FY+1E | Net income (GAAP) | 488.2 | 217.4% | 8 | 319.9 / 695.7 |

| FY+1E | Net income (normalized) | 478.6 | 82.3% | — | — / — |

| FY+1E | EPS (GAAP) | 8.34 | 150.9% | 8 | 1.46 / 12.62 |

| FY+1E | EPS (normalized) | 9.29 | 80.1% | 19 | 3.50 / 13.50 |

| FY+1E | Free cash flow | 769.6 | -58.6% | — | — / — |

| FY+1E | Dividend per share | 0.00 | — | — | — / — |

| FY+1E | Gross margin | 12.6% | 2.3% | — | — / — |

| FY+1E | Capital expenditure | -151.5 | 16.8% | — | — / — |

| FY+1E | Net debt | -1,854 | 41.0% | — | — / — |

| FY+1E | Cash from operations | 707.6 | -32.3% | — | — / — |

| FY+1E | ROE | 10.0% | 65.3% | — | — / — |

| FY+2E | Revenue | 50,434 | 6.1% | 10 | 46,498 / 55,410 |

| FY+2E | EBITDA | 1,107 | 14.8% | 7 | 869.4 / 1,274 |

| FY+2E | EBIT | 1,077 | 26.9% | — | — / — |

| FY+2E | Net income (GAAP) | 572.1 | 17.2% | 6 | 400.4 / 803.0 |

| FY+2E | Net income (normalized) | 650.7 | 36.0% | — | — / — |

| FY+2E | EPS (GAAP) | 11.46 | 37.4% | 5 | 7.85 / 15.74 |

| FY+2E | EPS (normalized) | 12.93 | 39.1% | 13 | 9.65 / 16.70 |

| FY+2E | Free cash flow | 1,145 | 48.8% | — | — / — |

| FY+2E | Dividend per share | 0.00 | — | — | — / — |

| FY+2E | Gross margin | 12.9% | 1.8% | — | — / — |

| FY+2E | Capital expenditure | -165.4 | 9.1% | — | — / — |

| FY+2E | Net debt | -2,531 | 36.5% | — | — / — |

| FY+2E | Cash from operations | 911.7 | 28.8% | — | — / — |

| FY+2E | ROE | 10.8% | 8.7% | — | — / — |

| Q2 FY2026 | Revenue | 10,781 | -5.7% | 13 | 10,218 / 11,056 |

| Q2 FY2026 | EBITDA | 174.0 | -61.3% | 7 | 158.2 / 197.9 |

| Q2 FY2026 | EBIT | 144.2 | -67.2% | — | — / — |

| Q2 FY2026 | Net income (GAAP) | 60.23 | -76.4% | 8 | 44.00 / 89.20 |

| Q2 FY2026 | Net income (normalized) | 74.74 | -74.6% | — | — / — |

| Q2 FY2026 | EPS (GAAP) | 1.25 | -73.6% | 6 | 0.87 / 1.75 |

| Q2 FY2026 | EPS (normalized) | 1.40 | -74.4% | 18 | 0.98 / 2.04 |

| Q2 FY2026 | Free cash flow | -82.00 | -130.6% | — | — / — |

| Q2 FY2026 | Dividend per share | 0.00 | — | — | — / — |

| Q2 FY2026 | Gross margin | 12.2% | -17.1% | — | — / — |

| Q2 FY2026 | Capital expenditure | -33.45 | 3.2% | — | — / — |

| Q2 FY2026 | Net debt | -1,803 | 26.5% | — | — / — |

| Q2 FY2026 | ROE | 7.5% | -70.9% | — | — / — |

| Q2 FY2026 | Cash from operations | -312.1 | -226.9% | — | — / — |

| Q3 FY2026 | Revenue | 10,901 | -5.0% | 13 | 10,207 / 11,271 |

| Q3 FY2026 | EBITDA | 174.2 | -5.8% | 7 | 136.3 / 221.5 |

| Q3 FY2026 | EBIT | 141.5 | -54.6% | — | — / — |

| Q3 FY2026 | Net income (GAAP) | 51.25 | -35.1% | 8 | 30.05 / 81.51 |

| Q3 FY2026 | Net income (normalized) | 58.46 | -71.9% | — | — / — |

| Q3 FY2026 | EPS (GAAP) | 1.05 | -30.3% | 6 | 0.59 / 1.59 |

| Q3 FY2026 | EPS (normalized) | 1.27 | -31.1% | 18 | 0.73 / 1.92 |

| Q3 FY2026 | Free cash flow | 123.0 | -25.0% | — | — / — |

| Q3 FY2026 | Dividend per share | 0.00 | — | — | — / — |

| Q3 FY2026 | Gross margin | 12.3% | -11.4% | — | — / — |

| Q3 FY2026 | Capital expenditure | -33.92 | 3.1% | — | — / — |

| Q3 FY2026 | Net debt | -1,876 | 48.6% | — | — / — |

| Q3 FY2026 | ROE | 8.7% | -48.4% | — | — / — |

| Q3 FY2026 | Cash from operations | 194.4 | 56.7% | — | — / — |

| Q4 FY2026 | Revenue | 11,843 | 4.1% | 13 | 11,064 / 12,640 |

| Q4 FY2026 | EBITDA | 107.6 | -198.7% | 6 | 55.38 / 139.0 |

| Q4 FY2026 | EBIT | 65.39 | -1.9% | — | — / — |

| Q4 FY2026 | Net income (GAAP) | -7.93 | -95.0% | 8 | -73.51 / 22.54 |

| Q4 FY2026 | Net income (normalized) | 6.39 | -41.5% | — | — / — |

| Q4 FY2026 | EPS (GAAP) | -0.14 | -95.4% | 6 | -1.44 / 0.42 |

| Q4 FY2026 | EPS (normalized) | 0.13 | -104.7% | 18 | -1.15 / 0.85 |

| Q4 FY2026 | Free cash flow | 409.0 | — | — | — / — |

| Q4 FY2026 | Dividend per share | 0.00 | — | — | — / — |

| Q4 FY2026 | Gross margin | 11.4% | 6.9% | — | — / — |

| Q4 FY2026 | Capital expenditure | -36.17 | 11.5% | — | — / — |

| Q4 FY2026 | Net debt | -2,122 | 306.4% | — | — / — |

| Q4 FY2026 | Cash from operations | 174.6 | -893.5% | — | — / — |

| Q4 FY2026 | ROE | -1.1% | -169.2% | — | — / — |

| Q1 FY2027 | Revenue | 11,389 | 5.5% | 6 | 10,612 / 12,229 |

| Q1 FY2027 | EBITDA | 290.6 | 77.2% | 5 | 235.3 / 396.4 |

| Q1 FY2027 | EBIT | 271.6 | 53.9% | — | — / — |

| Q1 FY2027 | Net income (GAAP) | 158.3 | 1030.5% | 5 | 113.6 / 232.4 |

| Q1 FY2027 | Net income (normalized) | 177.2 | 78.7% | — | — / — |

| Q1 FY2027 | EPS (GAAP) | 3.04 | 1027.0% | 4 | 2.23 / 4.58 |

| Q1 FY2027 | EPS (normalized) | 2.96 | 26.0% | 11 | 1.98 / 4.79 |

| Q1 FY2027 | Dividend per share | 0.00 | — | — | — / — |

| Q1 FY2027 | Gross margin | 13.2% | 11.3% | — | — / — |

| Q1 FY2027 | Capital expenditure | -40.76 | 23.5% | — | — / — |

| Q1 FY2027 | Net debt | -2,175 | 277.5% | — | — / — |

| Q1 FY2027 | ROE | 23.0% | 153.7% | — | — / — |

| Q1 FY2027 | Cash from operations | 177.0 | -76.8% | — | — / — |

Estimate momentum

Those reductions largely predate the last 30 days, over which both years' revenue and EPS have been broadly stable to slightly higher.

Currency: USD · Scale: money in millions, absolute (per share) · Point-in-time consensus; analyst count is shown where supplied.

| Period | Metric | Lookback | Then | Now | Direction / magnitude | Analysts |

|---|---|---|---|---|---|---|

| 2028 | Revenue | 30d | 49,540 | 50,434 | up 1.8% | — |

| 2028 | Revenue | 90d | 49,155 | 50,434 | up 2.6% | — |

| 2028 | Revenue | 180d | 52,122 | 50,434 | down 3.2% | — |

| 2027 | EPS (normalized) | 30d | 9.26 | 9.29 | up 0.3% | — |

| 2027 | EPS (normalized) | 90d | 8.20 | 9.29 | up 13.4% | — |

| 2027 | EPS (normalized) | 180d | 16.34 | 9.29 | down 43.1% | — |

| 2027 | Revenue | 30d | 47,249 | 47,524 | up 0.6% | — |

| 2027 | Revenue | 90d | 46,671 | 47,524 | up 1.8% | — |

| 2027 | Revenue | 180d | 50,371 | 47,524 | down 5.7% | — |

| 2028 | EPS (normalized) | 30d | 12.34 | 12.93 | up 4.8% | — |

| 2028 | EPS (normalized) | 90d | 12.51 | 12.93 | up 3.4% | — |

| 2028 | EPS (normalized) | 180d | 25.09 | 12.93 | down 48.4% | — |

Beat / miss record

Current sequences by metric: Revenue: 1 consecutive miss; EPS (normalized): 1 consecutive beat.

Currency: USD · Scale: money in millions, absolute (per share) · Consensus is captured before each actual first became effective; analyst count shown per observation.

| Quarter | Metric | Consensus as of | Actual | Surprise | Outcome | Analysts |

|---|---|---|---|---|---|---|

| Q1 FY2026 | Revenue | 10,886 | 10,796 | -0.8% | Miss | — |

| Q1 FY2026 | EPS (normalized) | 1.91 | 2.35 | 23.0% | Beat | — |

| Q4 FY2025 | Revenue | 10,905 | 11,375 | 4.3% | Beat | — |

| Q4 FY2025 | EPS (normalized) | 0.33 | -2.75 | -921.5% | Miss | — |

| Q3 FY2025 | Revenue | 10,984 | 11,477 | 4.5% | Beat | — |

| Q3 FY2025 | EPS (normalized) | 3.89 | 1.84 | -52.7% | Miss | — |

| Q2 FY2025 | Revenue | 10,941 | 11,427 | 4.4% | Beat | — |

| Q2 FY2025 | EPS (normalized) | 5.53 | 5.48 | -0.9% | Miss | — |

| Q1 FY2025 | Revenue | 10,814 | 11,147 | 3.1% | Beat | — |

| Q1 FY2025 | EPS (normalized) | 5.96 | 6.08 | 2.1% | Beat | — |

| Q4 FY2024 | Revenue | 10,319 | 10,499 | 1.7% | Beat | — |

| Q4 FY2024 | EPS (normalized) | 5.88 | 5.05 | -14.2% | Miss | — |

| Q3 FY2024 | Revenue | 9,912 | 10,340 | 4.3% | Beat | — |

| Q3 FY2024 | EPS (normalized) | 5.94 | 6.01 | 1.1% | Beat | — |

| Q2 FY2024 | Revenue | 9,754 | 9,880 | 1.3% | Beat | — |

| Q2 FY2024 | EPS (normalized) | 5.68 | 5.86 | 3.2% | Beat | — |

Where the street disagrees

Currency: USD · Scale: money in millions, absolute (per share) · Dispersion is high-low divided by absolute mean; analyst count shown per item.

| Period | Metric | Mean | Low | High | Spread / mean | Analysts |

|---|---|---|---|---|---|---|

| Q4 FY2026 | EPS (normalized) | 0.13 | -1.15 | 0.85 | 1563.0% | 18 |

| Q4 FY2026 | EPS (GAAP) | -0.14 | -1.44 | 0.42 | 1287.7% | 6 |

| Q4 FY2026 | Net income (GAAP) | -7.93 | -73.51 | 22.54 | 1210.8% | 8 |

| Q4 FY2025 | Net income (GAAP) | -5.11 | -34.71 | 15.00 | 973.5% | 7 |

| Q4 FY2025 | EPS (GAAP) | -0.17 | -0.68 | 0.15 | 478.2% | 5 |

Source: Visible Alpha consensus via S&P Xpressfeed · Consensus as of 2026-07-14 · generated 2026-07-17.

Model trust

This reads as a broad, timely consensus rather than a narrow or stale one.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Coverage depth and vintage; broker count is the maximum represented.

| Brokers | Line items | Last revision |

|---|---|---|

| 14 | 314 | 2026-07-14 |

Operating KPIs

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · FY-1A / FY0E / FY+1E; broker count shown per KPI.

| Operating KPI | Source | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|---|

| General and administrative expenses | CD | 2,952,707.24bn Amount | 2,906,178.34bn Amount | 3,092,677.69bn Amount | 14 |

| Medical care costs | CD | 39,071,602.51bn Amount | 38,951,976.71bn Amount | 42,418,451.87bn Amount | 14 |

| Premium revenue | CD | 42,779,644.46bn Amount | 42,105,377.33bn Amount | 46,042,367.97bn Amount | 14 |

| Premium tax expenses | CD | 1,724,224.62bn Amount | 2,023,000.07bn Amount | 2,033,030.93bn Amount | 14 |

| Depreciation and amortization | CD | 198,992.73bn Amount | 166,937.45bn Amount | 179,809.03bn Amount | 13 |

| General and Administrative Expenses - Operating | CD | 2,923,424.96bn Amount | 2,876,538.47bn Amount | 3,098,461.35bn Amount | 13 |

| General and administrative ratio - Operating(%) | CD | 6.5% | 6.4% | 6.3% | 13 |

| General and administrative ratio(%) | CD | 6.6% | 6.5% | 6.4% | 13 |

| Medical cost ratio - Life and Health Insurance(%) | CD | 91.3% | 92.5% | 92.1% | 13 |

| Medical cost ratio(%) | CD | 91.3% | 92.5% | 92.1% | 13 |

| Medical margin | CD | 3705588222.4% | 3158867777.5% | 3659974284.4% | 13 |

| Premium Revenue - Marketplace | CD | 4,576,880.29bn Amount | 2,666,145.20bn Amount | 2,609,649.79bn Amount | 13 |

P&L bridge

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Margins are derived against revenue; YoY compares adjacent fiscal columns; broker count shown per line.

| P&L line | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|

| Revenue | 45,030,856.77bn Amount | 44,588,465.14bn Amount (-1.0% YoY) | 48,554,889.24bn Amount (8.9% YoY) | 14 |

| Gross Profit | 5,955,852.13bn Amount (13.2% margin) | 5,636,488.43bn Amount (12.6% margin; -5.4% YoY) | 6,136,437.37bn Amount (12.6% margin; 8.9% YoY) | 14 |

| Ebitda | 1,220,414.75bn Amount (2.7% margin) | 682,445.22bn Amount (1.5% margin; -44.1% YoY) | 973,223.29bn Amount (2.0% margin; 42.6% YoY) | 12 |

| Operating Income | 1,093,858.88bn Amount (2.4% margin) | 522,112.47bn Amount (1.2% margin; -52.3% YoY) | 859,378.39bn Amount (1.8% margin; 64.6% YoY) | 11 |

| Net Income | 742,008.42bn Amount (1.6% margin) | 263,464.94bn Amount (0.6% margin; -64.5% YoY) | 480,672.20bn Amount (1.0% margin; 82.4% YoY) | 14 |

| Eps | 13.95 Amount | 5.17 Amount (-62.9% YoY) | 9.94 Amount (92.1% YoY) | 14 |

Consensus dispersion

The debate is therefore about how deep and durable the earnings trough proves, not about premium growth or the reported cost ratio.

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Top high-low spreads relative to absolute mean; requires at least 3 brokers.

| Line item | Period | Mean | Min | Q1 | Q3 | Max | Spread / mean | Brokers |

|---|---|---|---|---|---|---|---|---|

| EPS Diluted, Applicable to common stockholders($) | 4QFY-2026 | 0.11 Amount | -1.15 Amount | -0.07 Amount | 0.44 Amount | 0.85 Amount | 1892.6% | 14 |

| Net income/(loss), Applicable to common stockholders | 4QFY-2026 | 5,415.86bn Amount | -58,780.73bn Amount | -3,455.96bn Amount | 22,248.10bn Amount | 43,374.80bn Amount | 1886.2% | 14 |

| EPS Diluted, Applicable to common stockholders($) | 4QFY-2025 | 0.35 Amount | -0.33 Amount | 0.35 Amount | 0.42 Amount | 0.86 Amount | 339.1% | 12 |

| Net income/(loss), Applicable to common stockholders | 4QFY-2025 | 18,036.50bn Amount | -16,882.48bn Amount | 17,723.69bn Amount | 22,072.52bn Amount | 43,860.08bn Amount | 336.8% | 12 |

| Operating income/(loss) | 4QFY-2026 | 60,115.85bn Amount | -30,146.79bn Amount | 54,469.81bn Amount | 81,828.32bn Amount | 101,726.30bn Amount | 219.4% | 11 |

| Depreciation and amortization | 1QFY-2026 | 52,179.17bn Amount | 35,854.85bn Amount | 45,104.96bn Amount | 50,222.90bn Amount | 107,500.00bn Amount | 137.3% | 12 |

Quarterly path

Base currency: USD · VA scales normalized from Abs, M; item currencies and units retained · Next four supplied quarters; final column is maximum broker coverage in the row.

| Quarter | General and administrative expenses | Medical care costs | Premium revenue | Premium tax expenses | Depreciation and amortization | Total revenue | EPS Diluted, Applicable to common stockholders($) | Broker coverage |

|---|---|---|---|---|---|---|---|---|

| 3QFY-2026 | 688,498.98bn Amount | 9,602,838.09bn Amount | 10,356,524.10bn Amount | 498,747.53bn Amount | 41,875.33bn Amount | 10,972,436.66bn Amount | 1.27 Amount | 14 |

| 4QFY-2026 | 740,368.84bn Amount | 10,581,440.72bn Amount | 11,303,521.10bn Amount | 542,415.13bn Amount | 43,529.23bn Amount | 11,964,380.95bn Amount | 0.11 Amount | 14 |

| 1QFY-2027 | 800,985.96bn Amount | 10,207,405.38bn Amount | 11,195,513.01bn Amount | 495,546.60bn Amount | 44,208.91bn Amount | 11,810,959.59bn Amount | 3.16 Amount | 13 |

| 2QFY-2027 | 753,578.44bn Amount | 10,447,532.79bn Amount | 11,344,085.32bn Amount | 483,877.07bn Amount | 45,782.89bn Amount | 11,949,102.00bn Amount | 2.53 Amount | 13 |

38 stale period values omitted; 2 line items fully removed.

Source: S&P Capital IQ transcripts via Xpressfeed · latest indexed call 2026-04-23 · generated 2026-07-17.

Latest call digest

Molina Healthcare, Inc., Q1 2026 Earnings Call, Apr 23, 2026 · 2026-04-23T12:00:00

Q1 2026 — reported April 23, 2026. Molina posted adjusted EPS of $2.35 on $10.2 billion of premium revenue, a 91.1% consolidated MCR and a 1.6% adjusted pretax margin. By segment, Medicaid ran a 92% MCR (January rate updates in line, trend modestly favorable), Medicare 89.8% (the newly converted FIDE/HIDE duals products off to a good start), and Marketplace 84% on 305,000 members after the deliberate exposure cut.

The prepared remarks and the Q&A diverged on one point: management called the quarter "solid" and modestly favorable, yet only reaffirmed full-year guidance of approximately $42 billion of premium and at least $5 of adjusted EPS rather than raising it. Full-year segment assumptions were left unchanged — Medicaid MCR 92.9% (4% rates, 5% trend), Medicare 94%, Marketplace 85.5%, G&A ~6.4%, with roughly two-thirds of earnings weighted to the first half and Florida CMS implementation weighing on the fourth quarter.

The Q&A was dominated by two pressures: whether the assumption of no further acuity shift is credible now that low-and-no-utilizers sit at the lowest level Molina has recorded, and why guidance was not raised. Management repeatedly invoked a "time tested" preference for two quarters of data after 2025's volatility. The one guidance change surfaced in Q&A: same-store Medicaid attrition was lifted from a 2% to a 6% decline (California, Illinois, New York, Texas — California driven by the undocumented-immigrant population), with the revenue loss offset by higher Marketplace revenue so premium is unchanged. A May 8 Investor Day was flagged for the 2029 outlook.

Participant coverage from the latest call.

| Group | Participants | Count |

|---|---|---|

| Management | Operator; Jeffrey Geyer — Head of Investor Relations, Molina Healthcare, Inc.; Joseph Zubretsky — President, CEO & Director, Molina Healthcare, Inc.; Mark Keim — Senior EVP, CFO & Treasurer, Molina Healthcare, Inc. | 4 |

| Analysts | Andrew Mok — Director, Barclays Bank PLC, Research Division; Stephen Baxter — Senior Equity Analyst, Wells Fargo Securities, LLC, Research Division; Ann Hynes — Managing Director of Americas Research & Senior Healthcare Services Equity Analyst, Mizuho Securities USA LLC, Research Division; Kevin Fischbeck — Managing Director in Equity Research, BofA Securities, Research Division; Justin Lake — MD & Senior Healthcare Services Analyst, Wolfe Research, LLC; Sarah James — Research Analyst, Cantor Fitzgerald & Co., Research Division; Albert Rice — Health Care Services Analyst, UBS Investment Bank, Research Division; Scott Fidel — Research Analyst, Goldman Sachs Group, Inc., Research Division; John Stansel — Analyst, JPMorgan Chase & Co, Research Division; Erin Wilson Wright — Equity Analyst, Morgan Stanley, Research Division; Ryan Langston — Director & Senior Analyst, TD Cowen, Research Division; Hua Ha — Senior Research Analyst, Robert W. Baird & Co. Incorporated, Research Division; Lance Wilkes — Senior Analyst, Bernstein Institutional Services LLC, Research Division; George Hill — MD & Equity Research Analyst, Deutsche Bank AG, Research Division; Jason Cassorla — VP & Equity Research Analyst, Guggenheim Securities, LLC, Research Division | 15 |

Curated latest-call exchanges; one row per analyst topic.

| Analyst | Firm | Topic | What changed in Q&A |

|---|---|---|---|

| Andrew Mok | Barclays | Higher Medicaid attrition | Pressed which states drive the incremental membership pressure; management named California, Illinois, New York and Texas, with California tied to the undocumented-immigrant population, and argued no associated acuity shift. |

| Stephen Baxter | Wells Fargo | Acuity-shift assumption | Questioned whether zero further acuity shift is a reasonable baseline given how tightly enrollment is now managed; management pointed to low/no-utilizers at their lowest recorded level and stayer/leaver ratios near portfolio average. |

| Kevin Fischbeck | BofA Securities | Why guidance not raised | Asked whether holding guidance is routine Q1 caution or reflects real unquantifiable unknowns; management said the indicators are positive but a two-quarter, time-tested base is prudent after 2025's volatility. |

| Justin Lake | Wolfe Research | Medicaid trend composition | Sought quarterly trend figures and the acuity-versus-core split by cost category; management gave pure-period color but declined a clean quarterly breakout, citing seasonality and noise. |

| Scott Fidel | Goldman Sachs | Medicare duals vs. exiting MAPD | Asked to parse continuing duals MCR from the MAPD book being exited; management framed the 2027 duals-only structure and cited a ~$5.5 billion, ~94% MLR run rate. |

| Michael Ha | Baird | Low/no-utilizer definition | Pushed for the MLR buckets that define low utilizers; management declined to disclose the definition or absolute numbers, saying the directional decline holds across every definition tested. |

| George Hill | Deutsche Bank | 2027 work requirements | Asked how states will administer community-engagement/work requirements; management cited early-mover insight from Nebraska but flagged that CMS guidance on ex-parte and medical-frailty rules remains unclear. |

Theme tracker

Themes are curator-classified across supplied calls.

| Theme | Status | Quarters mentioned | Read-through |

|---|---|---|---|

| Medicaid rate/trend imbalance and market underfunding | persisted | Q3 2024, Q4 2024, Q1 2025, Q2 2025, Q3 2025, Q4 2025, Q1 2026 | The central margin debate. Framing hardened from 2023-early-2024's "actuarially sound" rates to a recurring claim that the managed-Medicaid market is 300-400 bps underfunded, with Molina positioned as best-in-class within it. Each 100 bps of Medicaid MCR is repeatedly tied to roughly $4.50-$5 of EPS, making rate restoration the key swing factor. |

| Redetermination acuity shift and low/no-utilizer analysis | persisted | Q2 2023, Q3 2023, Q4 2023, Q1 2024, Q3 2024, Q4 2024, Q1 2025, Q2 2025, Q3 2025, Q4 2025, Q1 2026 | Present every quarter but the tone inverted: "negligible" in 2023, a ~250 bps drag on 2025 trend, and now argued to be "largely behind us." The low/no-utilizer statistic and stayer/leaver analysis became the core evidentiary prop across the two most recent calls. |

| Marketplace de-risking and exposure reduction | emerged | Q2 2025, Q3 2025, Q4 2025, Q1 2026 | Emerged mid-2025 as enhanced-subsidy expiration and risk-pool volatility drove a ~30% average repricing, a ~20% county-footprint cut and a planned ~50% premium decline. A clear strategic reversal from the prior posture. |

| Marketplace as a growth engine funded by reinvested excess margin | dropped | Q4 2023, Q1 2024, Q2 2024, Q4 2024, Q1 2025 | Through early 2025 Molina touted two years of sub-target Marketplace MCRs (~75%) and reinvested "excess margin" to grow ~60%. That growth narrative disappeared as the segment pivoted to deliberate shrinkage — the dropped framing is itself signal about the risk pool. |

| Risk-corridor protection as a margin buffer | dropped | Q2 2023, Q3 2023, Q4 2023, Q1 2024, Q2 2024, Q3 2024, Q4 2024 | Corridors (~200 bps of protection) were a frequent talking point through 2024. By Q3 2025 protection was "very limited," and recent calls barely mention it — the cushion that muted early trend pressure has effectively lapsed from the story. |

| Medicare pivot to integrated duals (MMP to FIDE/HIDE) and MAPD exit | emerged | Q3 2024, Q4 2024, Q1 2025, Q3 2025, Q4 2025, Q1 2026 | The duals-integration transition built through 2024-2025 and crystallized into a decision to exit traditional MAPD for 2027, cited as a ~$1 EPS drag in 2026 that reverses. Positions Medicare as a duals-only franchise aligned with Medicaid integration. |

| Embedded earnings as forward value marker | persisted | Q2 2023, Q3 2023, Q4 2023, Q1 2024, Q2 2024, Q3 2024, Q4 2024, Q1 2025, Q2 2025, Q3 2025, Q4 2025, Q1 2026 | A fixture every call, growing from ~$4 to greater than $11 per share as RFP wins (Georgia, Texas, the $6bn Florida CMS contract) and acquisitions accumulated. Management leans on it to argue current depressed EPS understates franchise value. |

Guidance ledger

Quotes, calls, and speakers are source-verified; outcomes are curator-classified.

| Verbatim guidance | Call | Speaker | Curator outcome | Outcome note |

|---|---|---|---|---|

| “We project 2025 premium revenue of approximately $42 billion and adjusted earnings per share of at least $24.50” | Molina Healthcare, Inc., Q4 2024 Earnings Call, Feb 06, 2025 · 2025-02-06T13:00:00 | Joseph Zubretsky | missed | Full-year 2025 adjusted EPS ultimately came in at $11.03, less than half this initial guide, on 2025's Medicaid, Medicare and Marketplace trend pressure. |

| “Our full year 2025 adjusted earnings per share guidance is now expected to be approximately $14 per share” | Molina Healthcare, Inc., Q3 2025 Earnings Call, Oct 23, 2025 · 2025-10-23T12:00:00 | Joseph Zubretsky | missed | This mid-year cut (from a prior $19) still proved optimistic; the Q4 retro items in California and continued trend pressure took actual FY2025 adjusted EPS to $11.03. |

| “we are well on our way to meeting our target of $46 billion of premium revenue in 2026 and at least $52 billion in 2027” | Molina Healthcare, Inc., Q4 2024 Earnings Call, Feb 06, 2025 · 2025-02-06T13:00:00 | Joseph Zubretsky | missed | The $46 billion 2026 revenue target was withdrawn; 2026 premium is now guided to approximately $42 billion, chiefly on the planned Marketplace reduction and Georgia/Texas contracts slipping to 2027. |

| “Our 2026 adjusted earnings per share guidance is at least $5.” | Molina Healthcare, Inc., Q4 2025 Earnings Call, Feb 06, 2026 · 2026-02-06T13:00:00 | Joseph Zubretsky | pending | Reaffirmed on the Q1 2026 call despite a modestly favorable first quarter; management is holding rather than raising pending second-quarter results. |

| “In Medicaid, the full year MCR of 92.9% includes rate increases of 4% and medical cost trend at 5%.” | Molina Healthcare, Inc., Q1 2026 Earnings Call, Apr 23, 2026 · 2026-04-23T12:00:00 | Mark Keim | pending | Q1 2026 Medicaid ran a 92% MCR with trend modestly favorable, and management said Q1 annualized trend would land below 5%; the full-year outcome is not yet determinable. |

Q&A pressure map

Question counts and firms are curator tallies; analyst coverage shown above.

| Topic | Questions | Firms | Pressure / response |

|---|---|---|---|

| Acuity-shift risk and the low/no-utilizer assumption | 4 | Barclays, Wells Fargo, Baird, Deutsche Bank | The hardest-pressed topic on the latest call and a recurring one across 2025. Analysts repeatedly tested whether "no further acuity shift" holds now that enrollment is tightly managed. Management leaned on stayer/leaver data and the low/no-utilizer statistic but declined to disclose its definition or the underlying numbers, a non-disclosure worth flagging even though the thrust of each question was addressed. |

| Refusal to raise guidance after a favorable quarter | 3 | BofA Securities, Morgan Stanley, UBS | Analysts pushed on whether the caution signals specific unknowns; management consistently answered that nothing unusual occurred in Q1 and that a two-quarter, "time tested" base is simply prudent after 2025's volatility. |

| Medicaid cost-trend composition and cadence | 2 | Wolfe Research, Bernstein | Requests for quarterly trend figures and an acuity-versus-core split were met with pure-period color rather than a clean quarterly breakout, which management declined citing seasonality and noise. |

| Medicare duals economics ahead of the MAPD exit | 2 | Goldman Sachs, TD Cowen | Analysts sought run-rate visibility on the continuing duals book separate from the MAPD product being exited for 2027, and an update on efforts to transfer rather than wind down MAPD. |

Language shifts

Only language evidence verified against the referenced component is shown.

| Observation | Verbatim evidence | Call ID | Component |

|---|---|---|---|

| Baseline confidence before the deterioration: in early 2025 management framed long-term targets as firmly achievable, language that later gave way to loss-quarter caveats. | “remain very confident in our ability to achieve the long-term targets that we shared with you at our November Investor Day” | 1914754214 | 2 |

| New risk vocabulary entered the script as full-year 2025 results fell to an adjusted loss quarter — 2025 trend recast as an outlier rather than a new normal. | “We believe the medical cost trend in 2025 was an aberration, an anomaly by historical standards.” | 1975844137 | 2 |

| Introduction of explicit "trough" framing, positioning 2026 as the bottom of the Medicaid margin cycle rather than a further step down. | “We believe our 2026 forecast for Medicaid is the trough for managed Medicaid margins.” | 1975844137 | 2 |

| Even after a favorable quarter, prudence dominates over renewed confidence; guidance is treated as data-gated, echoing the repeated "time tested" refrain. | “merely reaffirming our prior full year guidance is a prudent approach at this early point in the year and in this current environment.” | 1986884066 | 2 |

The call history sets up a clean question. Management's thesis is that 2025's margin collapse was driven by a redetermination acuity shift that is now spent and by Medicaid rates that states will restore; Q1 2026 delivered the first data consistent with that. Unresolved is whether states close the claimed 300-400 bps of underfunding fast enough — and management's own refusal to raise guidance after a good quarter signals they want more proof too. The May 8 Investor Day and second-quarter results are the near-term arbiters.

Business and Thesis

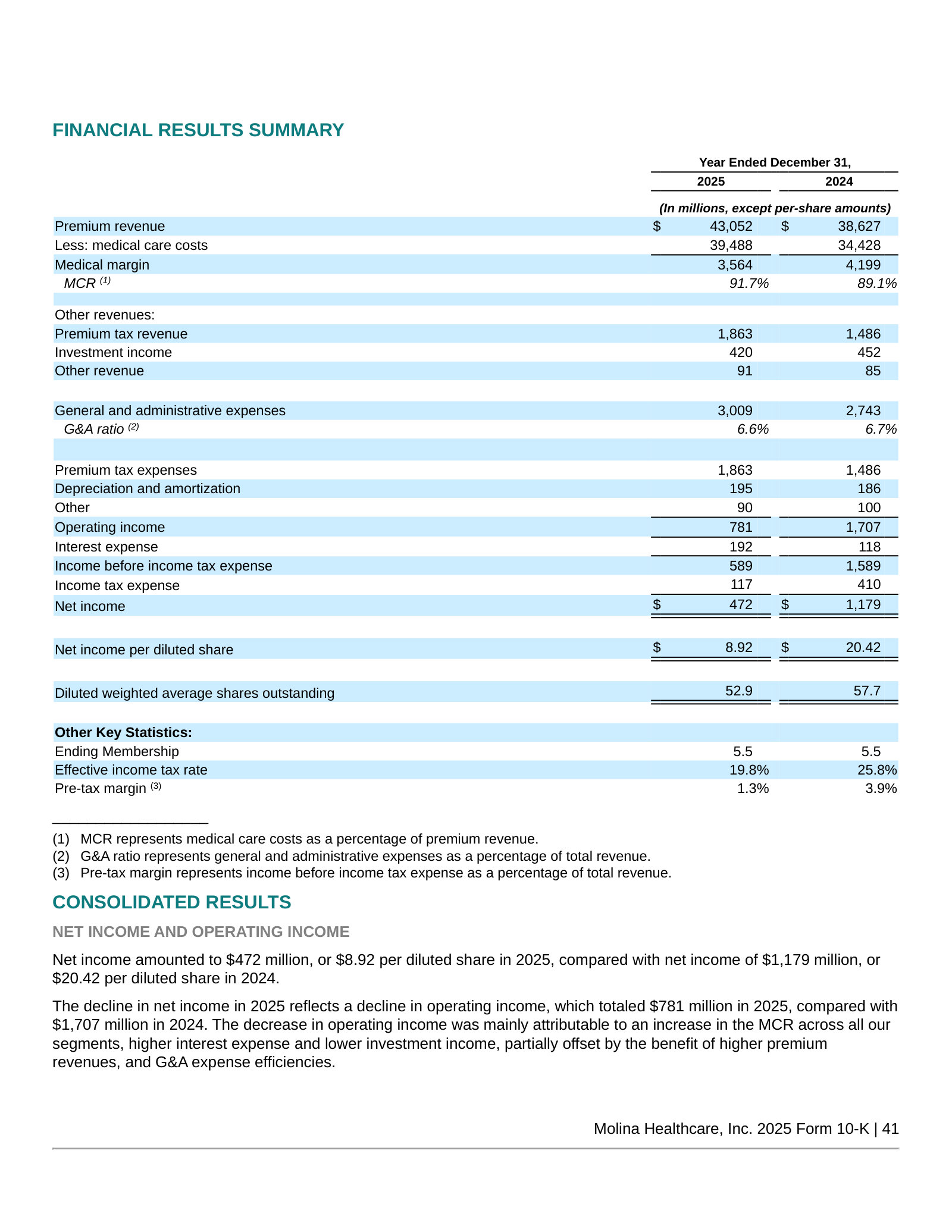

Molina Healthcare collects fixed monthly premiums from governments to run health plans for roughly 5.5 million low-income and elderly Americans, keeping the thin spread between those premiums and the medical claims it pays. Revenue has tripled since 2020, to $45.4 billion. But in 2025 the spread compressed sharply: the medical care ratio jumped to 91.7%, net income halved to $472 million, and the stock fell more than 60% from its peak. Everything that follows examines whether that break is temporary.

What Molina is

Molina is a pure-play government managed-care company. It contracts with state Medicaid agencies, with the federal Medicare program, and with the Affordable Care Act insurance marketplaces to arrange health care for people enrolled in those programs, operating across 21 states with about 5.5 million members at the end of 2025 [1]. It sells nothing to consumers directly and takes no commercial-employer risk; its customers are governments, and its revenue is other people's health-care budgets.

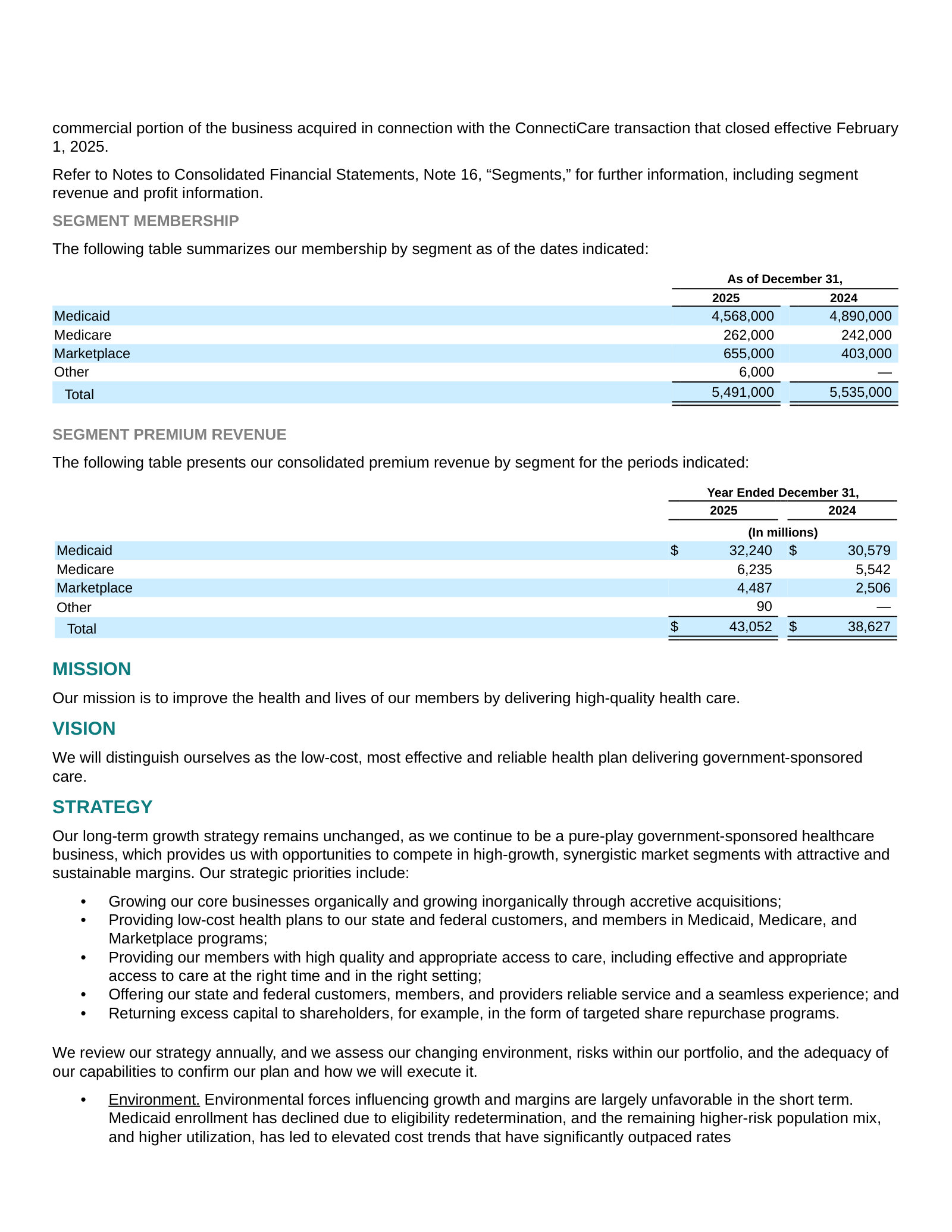

The business is heavily weighted to Medicaid, the joint federal-state program for low-income families. Medicaid supplied $32.2 billion of 2025 premium revenue against $6.2 billion from Medicare and $4.5 billion from the marketplaces — roughly three of every four premium dollars come from state Medicaid contracts [2].

Source: FY2025 Form 10-K segment revenue disclosures [3].

How it makes money

The economics are simple to state and hard to run. A state pays Molina a fixed per-member, per-month (PMPM) rate, set annually and required to be actuarially sound; in return, Molina assumes the medical and administrative cost risk for those members [4]. Molina keeps whatever premium is left after paying claims and running the plan. Because premiums are fixed by contract for the year while medical costs are not, the margin is set almost entirely by one ratio — the share of each premium dollar consumed by medical claims. Molina calls it the medical care ratio (MCR); the rest of the industry calls it the medical loss ratio. In Molina's own words, if premiums do not rise as fast as medical costs and utilization, "our medical margins will be compressed or eliminated, and our earnings will be negatively affected" [5].